Qualcomm’s $166 test could set the tone for chips

Qualcomm has reached that awkward point after a good earnings report: the numbers were fine, yet the stock looks tired.

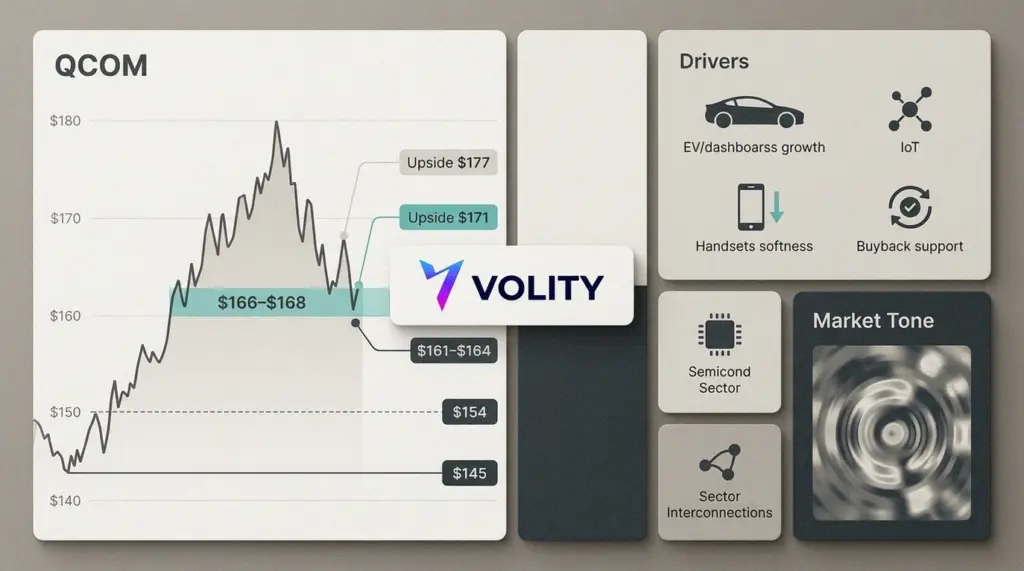

QCOM closed Monday at $168.38, down almost 5% on the day. That move erased much of the cheer from its post-results jump to $180.49. Now, traders are watching the $166 to $168 area with unusual care. If buyers defend it, the chip trade may steady. However, if it fails, the next leg lower could spread beyond Qualcomm.

The sell-off did not come from a broken business. Instead, it came from a colder view of future growth. Investors liked the earnings beat, but they disliked the message beneath it. Android demand in China remains soft. Handset recovery still looks patchy. Therefore, Qualcomm’s biggest business is no longer giving the market an easy story.

That matters because QCOM often acts like a weather vane for old and new semiconductor demand. It sells into smartphones, cars, connected devices and, increasingly, markets tied to edge computing. When the stock cannot hold a rally, traders tend to ask a wider question. Is this only Qualcomm’s problem, or a warning for the chip cycle?

The support zone

The most important level sits between $166 and $168. Chart traders see that band as the 0.618 retracement of the post-earnings advance. That sounds technical, but the point is simple. It is the place where dip-buyers should appear if confidence remains intact.

So far, the stock has bent rather than snapped. The 50-period moving average still rises below the market. Meanwhile, the relative strength index has cooled toward the mid-40s. That shows fading momentum, not panic.

However, the margin for error has narrowed. A break below $166 would put $161 to $164 in play. Below that, $154 becomes the next visible shelf. The 200-period moving average, near $145, remains the deeper structural line for longer-term bulls.

On the upside, $171 stands as the first obstacle. After that, $177 becomes more important, followed by the $180.49 post-earnings high. A move through those levels would suggest Monday’s drop was a sharp shakeout, not the start of a wider unwind.

By the numbers

- Monday close: $168.38, down nearly 5%.

- Post-earnings high: $180.49.

- Key support: $166 to $168, then $161 to $164.

- Automotive revenue: $1.33 billion, up 38% year over year.

- Buyback: new $20 billion repurchase authorisation.

The bull case

Qualcomm’s defence begins with diversification. The company is not just an Android handset parts supplier, even if the market still treats it that way during sell-offs.

Automotive revenue reached a record $1.33 billion, up 38% from a year earlier. That is not background noise. Cars now need more chips, more connectivity and more software-defined systems. Consequently, Qualcomm has found a growth lane outside the mature smartphone market.

The company also has a $45 billion automotive design-win pipeline. Those wins do not all become revenue tomorrow. Still, they give investors a line of sight into demand beyond the current handset cycle.

Meanwhile, the Internet of Things business grew 9%. That segment lacks the glamour of artificial intelligence servers, but it helps smooth the revenue mix. Connected devices, industrial hardware and edge systems all support a broader chip platform.

Valuation strengthens the bull case. QCOM trades around 17 times forward earnings. The wider semiconductor group trades much richer, near 35 times forward earnings. Broadcom, for example, stands above 30 times. Therefore, Qualcomm does not need a perfect story to look inexpensive.

The $20 billion buyback also helps. Management does not spend that kind of money casually. While buybacks cannot fix weak end-demand, they can support per-share earnings and signal confidence at lower prices.

The bear case

The problem sits in plain view. Handsets still matter most, and that business fell 13%. For Qualcomm, smartphones remain the engine room. When that room cools, the whole ship slows.

Android demand in China remains the sore point. Consumers there have not rushed back into premium devices. At the same time, memory pricing pressure and supply issues have clouded the recovery path. As a result, investors cannot simply pencil in a clean rebound.

Guidance did not calm every concern. Management pointed to revenue of $9.2 billion to $10.0 billion, which still implies growth. However, the pace looked less exciting than some traders wanted after the rally.

That explains Monday’s move. The market did not punish Qualcomm for missing the present. It punished the stock for making the future look less immediate.

There is another issue. The semiconductor trade has become crowded in the winners. Money has chased AI-linked names, infrastructure suppliers and anything tied to data-centre spending. Qualcomm has exposure there, but not enough to erase handset disappointment overnight.

The trade

For swing traders, the setup is clean. A long entry near $166 to $168 offers a defined risk line. A stop below $161 keeps losses contained if support fails.

The first target sits near $171. That offers only modest upside, but it gauges whether buyers remain active. A stronger rebound toward $177 would improve the reward profile. Moreover, a break above $180.49 would return control to the bulls.

Still, traders should not view the chart in isolation. If the Nasdaq weakens, chip stocks rarely stand apart for long. Sector selling can drag strong companies down with the weak ones. Therefore, QCOM’s level matters more if broader tech also finds support.

Position investors face a different choice. They can add slowly around support, but they must accept a longer wait. The real payoff depends on automotive growth, IoT durability and fresher traction in data-centre chips.

In other words, the stock offers value, but not instant proof.

Key takeaways

- Above $166: Bulls can argue the post-earnings pullback remains orderly.

- Below $161: Momentum likely shifts toward $154 and deeper sector selling.

- Above $177: The stock starts repairing the damage from Monday’s reversal.

- Watch handsets: China Android demand remains the key near-term earnings risk.

- Watch autos: The $45 billion pipeline drives the longer-term bull case.

The wider message

Qualcomm’s pullback is not a collapse. It is a test of what investors will pay for uneven growth.

The company has real strengths: automotive momentum, a broader product mix, a large buyback and a modest valuation. Yet it also has a stubborn weakness in handsets, where visibility remains poor.

That tension makes $166 to $168 more than a chart level. It is the market’s vote on whether investors still want reasonably priced chip stocks with imperfect stories. If QCOM holds there, the semiconductor tape could regain its footing. If it breaks, traders may start cutting exposure across the group.

For now, Qualcomm sits right on the line. The business looks better than the stock. However, in a nervous market, the stock gets the final word first.