This content is for informational purposes and does not constitute financial or investment advice. Trading Forex, Cryptocurrencies, or CFDs involves significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Please ensure you fully understand the risks involved and seek independent advice if necessary.

Why software will eat AI: the real enterprise AI story in 2026

The AI trade has been tidy for two years. First came chips, then models, then the promise of clever apps. However, 2026 is starting to look messier and more profitable for a different cohort. Software is not being replaced by AI. Instead, enterprise software is swallowing AI and turning it into an operating layer.

That sounds semantic, yet it changes who wins. Consumer AI sells wonder. Meanwhile, enterprise tech sells control. A global bank does not buy “insight”. It buys repeatable processing, permissions, routing, recordkeeping and audit trails. It also wants someone accountable at 3 a.m. Therefore, foundation models can be dazzling and still unusable, because they remain non-deterministic.

Boards keep learning the same, slightly boring lesson. The hard part is not writing code quickly. It is building architecture that survives regulation, edge cases, and decades of patchwork processes. Consequently, the idea that AI will “replace software” collapses the moment you look at the systems that run payroll, claims, compliance, revenue recognition, and procurement.

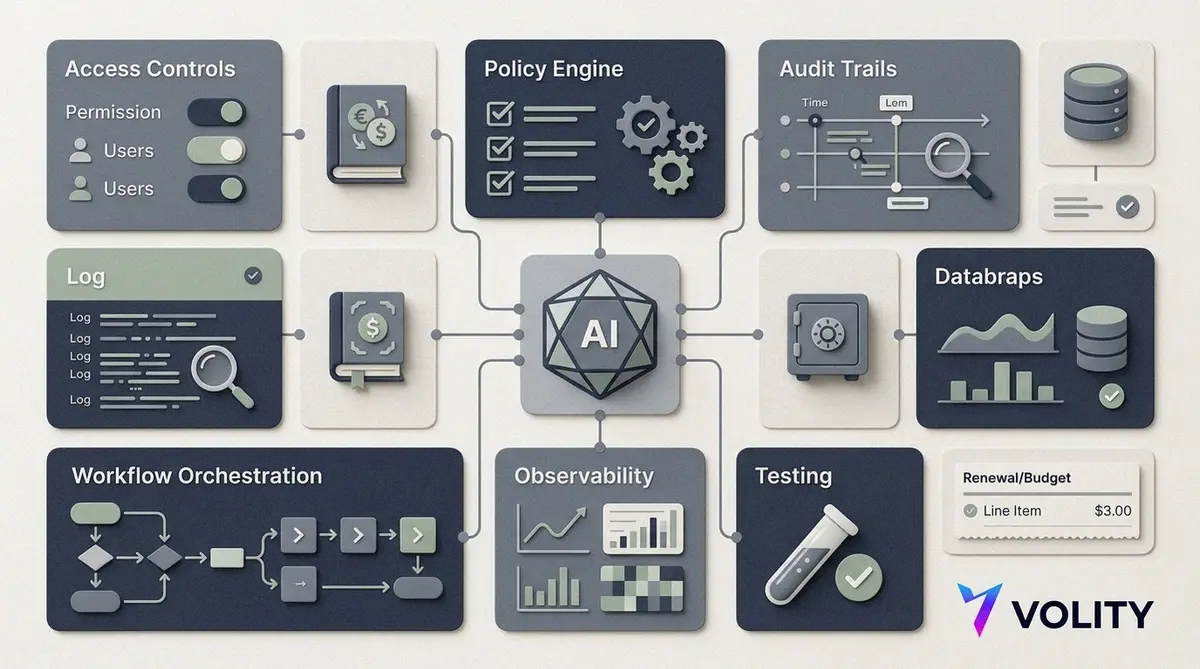

The architecture problem nobody likes to fund

Enterprise platforms are not just code bases. They are accumulated institutional memory. They include deeply embedded workflow logic, private domain data, granular access controls, resilience patterns, support models, and procurement relationships. Meanwhile, the distribution moat matters more than the demo.

This is why incumbents look calm in public and frantic in private. They do not need to scrap their platforms. Instead, they need to domesticate AI inside them, so the model works under enterprise constraints. That means observability, testing, validation, and policy controls. It also means pricing that procurement teams can live with.

The market is already voting with deployments

Microsoft says more than 80% of the Fortune 500 is deploying active agents built with low-code or no-code tools. That is not software disappearing. Rather, it is software becoming the control plane for agentic work.

Salesforce pushed this logic with Agentforce 2.0, framing it as digital labour that can take actions across workflows. More importantly, Salesforce has leaned into consumption pricing, including pay-per-action and pay-per-conversation. Therefore, AI shifts from “pilot theatre” into budget lines, renewal negotiations, and revenue reporting.

Oracle is arriving at the same destination by a different road. Its agents sit at the transaction layer in Fusion Applications, while its agent tooling adds the governance scaffolding enterprises demand. ServiceNow sends a similar message, because agents work inside a single trusted platform with unified data models and automation. Consequently, the winners are not unleashing free-range AI. They are penning it inside systems of record and systems of action.

Adoption is rising, yet scaling remains the gate

Worker access to AI rose by 50% in 2025, while the number of companies with at least 40% of projects in production is expected to double within six months. Meanwhile, forecasts now suggest 40% of enterprise software applications will include task-specific AI agents by end-2026, up from under 5% in 2025.

Yet the real tell is where AI lands. Firms are embedding it into procurement automation, customer service operations, finance and risk monitoring, software engineering, and operational support. In other words, they pick workflows that already have governance and ownership. However, although 78% of organisations now use AI, nearly two-thirds have not scaled it across the enterprise. The gap persists because scaling requires integration with permissions, accountability, and controls.

Valuations: the dull bits that matter

HSBC Global Research argued in February 2026 that legacy enterprise software vendors may be primary beneficiaries of AI diffusion, while valuations remain historically low relative to the opportunity. The claim is not that every software ticker becomes an AI winner. Instead, the upside clusters where installed bases are deep, workflow ownership is real, and monetisation is credible.

Therefore, the investor question has sharpened. It is no longer “Will AI replace software?” It is “Which software firms can absorb AI, constrain it, price it, and prove ROI?” That pushes attention towards distribution, trust, integration depth, domain specificity, and billing design. None of that is glamorous. All of it is decisive.

A side note from finance: the appeal of one operating layer

The same instinct explains why “borderless finance” stories are resonating. Volity’s pitch, an integrated account for investment, holding and payment, sells a vertically unified operating system. Users do not want intelligence scattered across disconnected tools. They want an operating layer that turns complexity into action. AI helps. Software still owns the job.

From infrastructure to orchestration

The first phase of AI rewarded infrastructure. Chips, training, and foundational tooling captured the early rent. The next phase is likely to reward orchestration, meaning the firms that can integrate AI reliably, govern it completely, and charge for it sustainably.

The durable winners will not be the companies with the smartest models. Rather, they will be the ones that make AI safe, auditable, and useful inside the software that already runs the modern enterprise.

By the numbers

- 80%+ of the Fortune 500 deploying active agents via low-code or no-code tools, per Microsoft

- 50% rise in worker access to AI during 2025

- 40% of enterprise software applications expected to include task-specific AI agents by end-2026

- <5% of enterprise applications had such agents in 2025

- 78% of organisations now use AI, yet nearly two-thirds have not scaled it enterprise-wide

Key takeaways

- Prefer software firms with workflow ownership and installed-base pricing power, not just AI branding.

- Watch for consumption models that tie AI to actions, because they pull spend into recurring budgets.

- Governance tooling is a revenue feature, since enterprises pay to make AI safe and auditable.

- Agent success will track integration depth, not model IQ.

- The “AI replaces software” trade is fading, while “software absorbs AI” is becoming the durable frame.