AI’s power trade moves from chips to sockets

AI has spent two years looking like a chip trade. Now it looks like a power trade too.

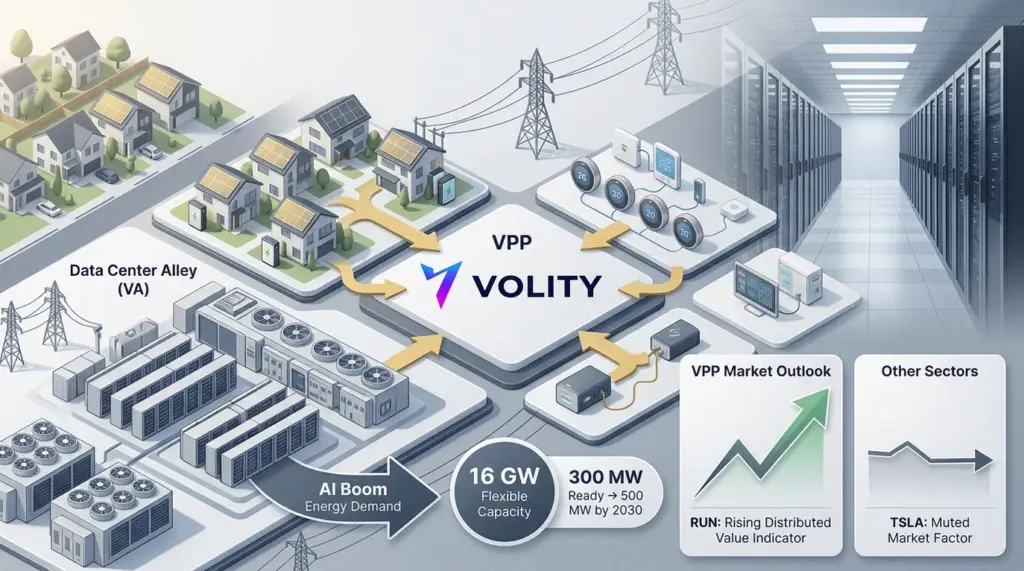

Sunrun, Tesla and Renew Home have pushed that point into the market’s lap. Their new virtual power plant plan would pool more than 16 gigawatts of flexible capacity. That means home batteries, rooftop solar and smart thermostats working as one dispatchable grid asset.

In Virginia’s Data Center Alley, the group says it already has 300 megawatts ready. It wants at least 500 megawatts there by 2030. For a region straining under server farms, that is not decorative green branding. It is capacity with a ticker attached.

Sunrun shares understood the message first. RUN jumped roughly 26 per cent to 30 per cent in one session, one of its biggest moves in years. However, the stock remains down for 2026, which keeps the trade combustible.

Tesla barely moved. That reaction makes sense. The deal helps its energy narrative, but TSLA still trades mainly on EV demand, autonomy hopes and broad tech risk. Sunrun, meanwhile, suddenly looks less like a bruised solar installer and more like a distributed-grid operator for AI customers.

Therefore, the next move in RUN will not depend only on the chart. Traders need confirmed data-centre contracts, utility approvals and capacity payments. They also need to watch PJM and state regulators, because virtual power plants live or die by dispatch rules.

By the numbers

- 16 GW – targeted flexible capacity across Sunrun, Tesla and Renew Home.

- 300 MW – capacity described as ready in Virginia’s Data Center Alley.

- 500 MW – minimum Virginia target by 2030.

- 26-30% – approximate one-day jump in RUN after the announcement.

- 2026 – Micron’s HBM supply is described as already sold out.

Micron’s memory shortage changes the old cycle

Further along the AI stack, Micron has become harder to dismiss as a plain commodity name.

The company’s high-bandwidth memory pipeline is the cleaner story. Micron says its HBM supply for 2026 is already sold out under fixed-price contracts. That gives unusual visibility for a business famous for brutal inventory swings.

Meanwhile, AI servers keep dragging DRAM and HBM demand higher. Scarcity lets Micron price memory more like critical infrastructure than shelf-stock semiconductors. Margins have followed, and guidance has carried more force than usual.

Analysts have crowded into the bullish camp, but that creates its own risk. A stock with heavy “Strong Buy” support needs only a small wobble in HBM pricing to punish late buyers. So the thesis is strong, but the tape will stay sharp.

Options traders already treat MU as an event stock. Earnings, capital-expenditure language and any comment on 2027 commitments can swing the shares hard. In practical terms, Micron is now both an AI infrastructure holding and a quarterly volatility machine.

For Nvidia and AMD, compute still sets the front-page story. However, Micron now controls one of the bottlenecks behind that story. AI cannot train faster if memory supply cannot keep up.

SanDisk is not a ghost trade

Storage adds a useful correction to the summer map. SanDisk should not be treated as a dead ticker in 2026.

Western Digital bought SanDisk in 2016. However, the flash business later returned to market as a separate SanDisk company under SNDK, while Western Digital kept the hard-disk-drive business under WDC.

That matters because traders need to compare the right exposures. MU offers cleaner AI memory leverage through DRAM and HBM. SNDK gives investors flash and NAND exposure. WDC leans more toward drives, cloud storage and data-centre capacity demand.

Consequently, “AI storage” is not one trade. It is three different balance sheets, three pricing cycles and three sets of earnings sensitivities.

Event stocks are setting traps and chances

Not every active name needs a grand AI story. Some simply need a catalyst and enough liquidity.

Bio-Techne (TECH) needs careful handling after takeover chatter linked to Merck KGaA and an enterprise value around $11.3 billion. If a signed all-cash deal arrives, the stock becomes merger arbitrage. The upside then becomes the spread, not blue-sky growth.

However, traders should separate reports from confirmed terms. Deal risk, antitrust scrutiny and official denials can turn a neat spread into a trap.

Elsewhere, BlackBerry (BB), McCormick (MKC), Worthington Steel (WS), Acuity Brands (AYI) and Yiren Digital (YRD) sit in post-earnings mode. Each name offers a different lever: cyber and IoT, spices, steel, lighting and Chinese fintech.

Yet the trading structure looks similar. Watch the second-day reaction, not just the headline beat. Guidance, margin language and short interest usually decide whether the gap holds.

At the speculative end, Tonix Pharmaceuticals (TNXP) has drawn fresh bullish coverage. Small biotech can move quickly on sentiment. Still, thin liquidity and financing risk demand ruthless position sizing.

Yield names keep their place

While AI stocks grab the screen, income trades have not disappeared. In energy infrastructure, Enterprise Products Partners (EPD) and Cheniere Partners (CQP) still offer yields north of 5 per cent.

These are not natural day-trading vehicles. However, their cash flows rest on pipelines, gas liquids and LNG export volumes. In a market arguing over rates, being paid to wait still has value.

Real estate also refuses to trade as one sleepy sector. Crown Castle (CCI) is a tower REIT, tied to wireless traffic and digital infrastructure. Braemar Hotels & Resorts (BHR) tracks travel demand and discretionary spending. Zillow (Z) behaves more like a housing-data and prop-tech equity than a yield instrument.

So the real-estate watchlist now splits into macro, travel and housing beta. That gives traders more choice, but also less protection from sloppy labels.

Index flows tie it together

The broader market has noticed the same pattern. Recent sessions have seen the Dow add roughly 250 points, with tech strength setting the tone. Micron’s AI outlook helped risk appetite, while the power-grid story gave traders a fresh angle.

For index users, SPY, QQQ and DIA now carry several overlapping trades. Continuation buyers need AI earnings, power demand and benign rates to keep working together. Fade traders need crowded positioning to meet a macro shock.

Either way, Micron’s guidance now speaks beyond one stock. Sunrun’s grid pitch does too. The market is learning that AI needs electricity before it needs more chips, and memory before it delivers more magic.

Key takeaways

- RUN is now an AI-power momentum name, not only a solar recovery trade.

- TSLA gains energy credibility, but EV and autonomy sentiment still dominate.

- MU remains a core AI bottleneck trade, with high earnings-event risk.

- SNDK, WDC and MU should not be lumped into one storage basket.

- SPY and QQQ increasingly reflect power, memory and AI capex expectations.