This content is for informational purposes and does not constitute financial or investment advice. Trading Forex, Cryptocurrencies, or CFDs involves significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Please ensure you fully understand the risks involved and seek independent advice if necessary.

Intel’s turnaround bet runs into its own valuation

Intel shares spent this week arguing with themselves. On one side sat a clean momentum trade. On the other sat the ugly arithmetic of a turnaround priced like a triumph.

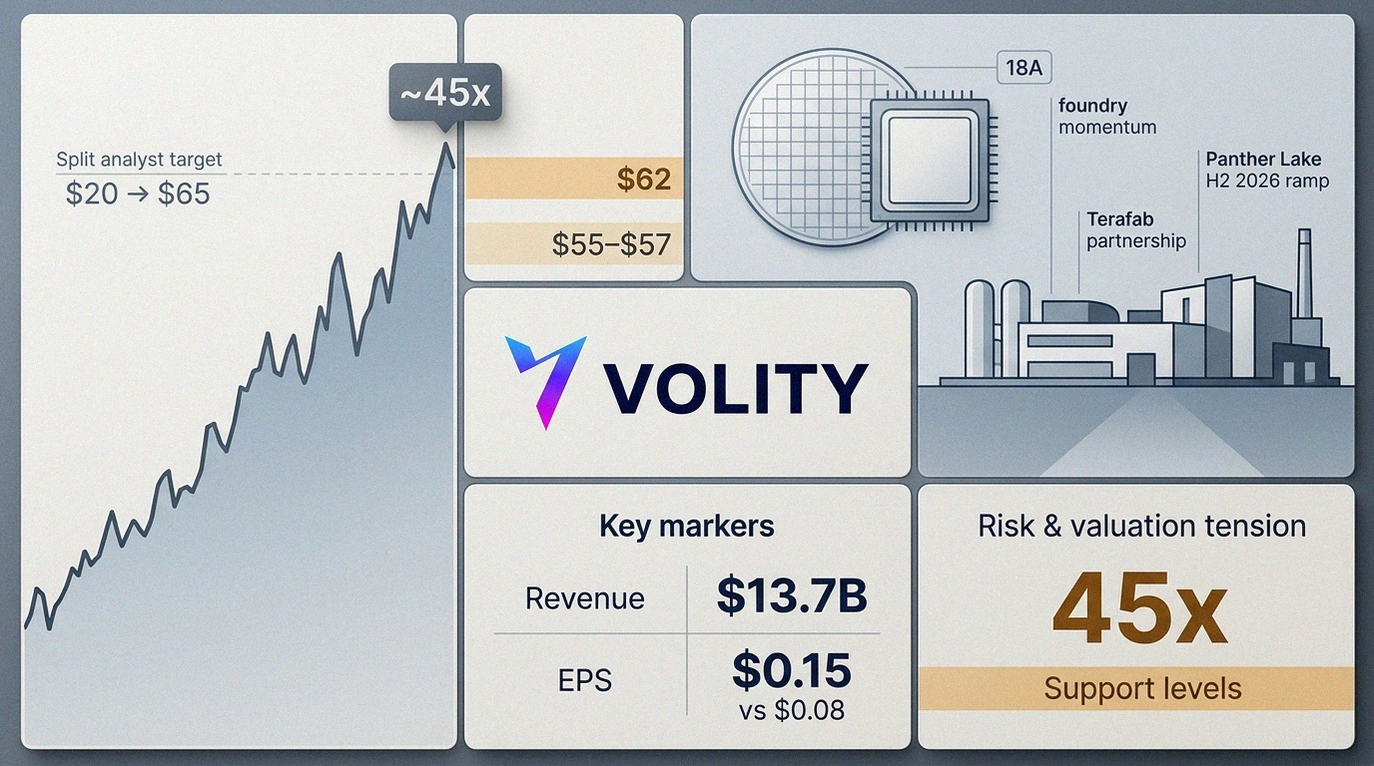

INTC traded around $64.86 after it snapped a nine session winning streak. Meanwhile, the stock is up about 31.8% since January 2026. That rise has not been pure vibes. However, it has pushed investors into a familiar corner: paying today for execution that still sits in tomorrow’s diary.

Lip-Bu Tan took over in March 2025 with a manufacturing mandate. He also arrived with a reputation for compounding, after his long run at Cadence. Therefore, the market has given Intel something it lacked for years: belief that the factory story might finally land.

Some proof has followed. Intel has talked up 18A progress and a ramp in foundry activity, while a high profile Terafab partnership story has helped reframe Intel as a builder again. Meanwhile, the company’s fourth quarter 2025 print gave bulls their first clean headline beat in a while.

Revenue came in at $13.7 billion and non-GAAP EPS printed at $0.15, above the $0.08 expectation. Those are not numbers that force anyone to rewrite models. However, they do matter in a stock that had started to trade like a stranded asset.

The options tape has matched the renewed confidence. Short put trades around the $64 strike implied a punchy yield, and call activity has stayed heavy on up days. Meanwhile, early week volume spiked, with roughly 12.6 million shares changing hands in the first 15 minutes of one session. That looked like repositioning, not a retail wobble.

Where the story creaks

Valuation has stopped being a footnote. At around 45.5 times earnings on the latest quarter’s run rate, Intel now asks investors to underwrite something close to best case execution. However, forward and “normalised” earnings measures look even more stretched, which is where the discomfort sets in.

Analysts have not lined up behind a single narrative. Consensus sits around Hold, yet published targets run from roughly $20 to $65. Therefore, the debate is not about one quarter’s demand. It is about whether Intel’s manufacturing reboot becomes durable, or just another expensive detour.

The bull checklist is clear. Intel needs Panther Lake to ramp cleanly in the second half of 2026. It also needs foundry orders to turn into reliable quarterly revenue north of $13.5 billion. Finally, it needs gross margin to lift towards 35% and keep climbing. Any one miss, however, will look large inside a multiple that already assumes progress.

Momentum traders have a map, but not a safety net

Technicals now show classic late sprint conditions: overbought readings alongside strong trend structure. Therefore, pullbacks can happen fast, even if the longer move remains intact.

The recent slip from about $65.18 to $62 reads like normal digestion after nine green sessions. Meanwhile, the market has started to define a near term line in the sand. Options pricing suggests support thinking sits near $62, while chart watchers keep circling the $55 to $57 zone as the next serious test.

That gap matters because Intel is no longer cheap enough to forgive stumbles. However, it is also no longer broken enough to ignore. The catalyst set is real, yet the stock now charges admission for outcomes, not hopes.

By the numbers

- Last trade area: about $64.86

- Year to date move: roughly +31.8% since January 2026

- Q4 2025 revenue: $13.7bn

- Q4 2025 non-GAAP EPS: $0.15 vs $0.08 expected

- Key levels traders cite: $62 near term, then $55 to $57

Key takeaways

- Momentum is intact, yet the stock now reacts sharply to any execution wobble.

- Options markets imply support around the low $60s, which may anchor dip buying.

- Valuation raises the bar, so “good” updates may not be enough to push shares higher.

- Watch margins, since gross margin recovery is the cleanest fundamental tell.

- Define risk first, because the debate is now about scale delivery, not direction.

Intel has made the turnaround trade tradable again. However, it has also made it expensive. The next leg will not be decided by speeches or partnerships. It will be decided by wafers, yields and margins, quarter after quarter.