This content is for informational purposes and does not constitute financial or investment advice. Trading Forex, Cryptocurrencies, or CFDs involves significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Please ensure you fully understand the risks involved and seek independent advice if necessary.

Starting to invest in stocks requires a clear path, especially with limited capital. This guide provides a direct, seven-step framework for beginners. It focuses on initial investments between $100 and $1,000, simplifying complex financial concepts and outlining realistic growth expectations.

While understanding Stocks Investing Basics is important, applying that knowledge is where the real growth happens. Create Your Free Forex Trading Account to practice with a free demo account and put your strategy to the test.

The Reality Check: Can You Start With Small Amounts?

Many new investors believe significant capital is necessary to begin. This perception often leads to inaction, delaying potential financial growth. In reality, starting with amounts as low as $100 is entirely feasible and offers substantial long-term benefits.

Brokerages widely offer fractional shares, enabling investors to purchase portions of high-priced stocks. This mechanism removes the barrier of needing hundreds or thousands of dollars for a single share.

For example, with a $100 investment, owning 0.1 share of a $1,000 company becomes possible. This approach provides immediate market exposure and starts the wealth accumulation process.

The Cost of Waiting vs. Starting Small

Delaying investment carries a tangible financial cost. Every year an investor waits, they miss opportunities for compound interest to grow their capital.

For instance, an investment growing at an average market rate of 10% annually doubles approximately every 7.2 years, according to the Rule of 72. Waiting a decade means forfeiting a doubling period.

Inflation vs. Investment Results

Inflation erodes purchasing power over time. The average annual inflation rate historically hovers around 3%. Money held in cash loses value against this rate.

Investing aims to beat inflation, with average stock market returns often exceeding it. This preserves and grows wealth, contrasting sharply with the guaranteed loss of value experienced by uninvested savings.

Understanding the Risks Before You Begin

All investing involves risk; stocks are no exception. Market values fluctuate based on economic news, company performance, and global events. Understanding these inherent risks prepares investors for volatility and prevents impulsive decisions. Equity markets experience periods of both growth and decline.

Market Volatility vs. Risk Tolerance

Market volatility describes price swings. Some investors tolerate higher volatility for potentially greater returns, while others prefer stability. Assessing personal risk tolerance helps determine appropriate investment choices.

Younger investors with longer time horizons often embrace more risk. Conversely, those closer to retirement typically prioritize capital preservation. Diversification across different assets also helps mitigate concentrated risk.

The Role of SIPC and Regulatory Protection

The Securities Investor Protection Corporation (SIPC) protects investors against brokerage firm failure, not market losses. SIPC coverage extends up to $500,000, including $250,000 for cash. This ensures assets are returned if a broker goes out of business.

This protection contrasts with bank FDIC insurance, which covers cash deposits. Regulatory bodies, like the SEC in the U.S., also oversee markets. They ensure fair practices and investor confidence.

How to Start Investing in Stocks in 7 Steps

Entering the stock market involves a structured process that simplifies the initial complexity. Beginners successfully navigate these steps to establish their investment path. This approach transforms the overwhelming task of “how to start” into actionable stages.

Step 1: Define Your Financial Goals

Clear financial goals guide investment decisions. Short-term goals, like a down payment in 3 years, require less volatile investments.

Long-term goals, such as retirement in 30 years, often benefit from aggressive growth strategies. Defining a specific target amount and timeframe provides a measurable objective. This clarity helps determine appropriate asset allocation.

Step 2: Decide How You Want to Invest

Investors select between actively managing their portfolio or using automated services. Do-it-yourself (DIY) investing offers full control but requires research and ongoing management. Robo-advisors automate portfolio creation and rebalancing based on risk tolerance. This provides a hands-off approach. Hybrid models also offer professional advice combined with self-management options.

Step 3: Open an Investment Account

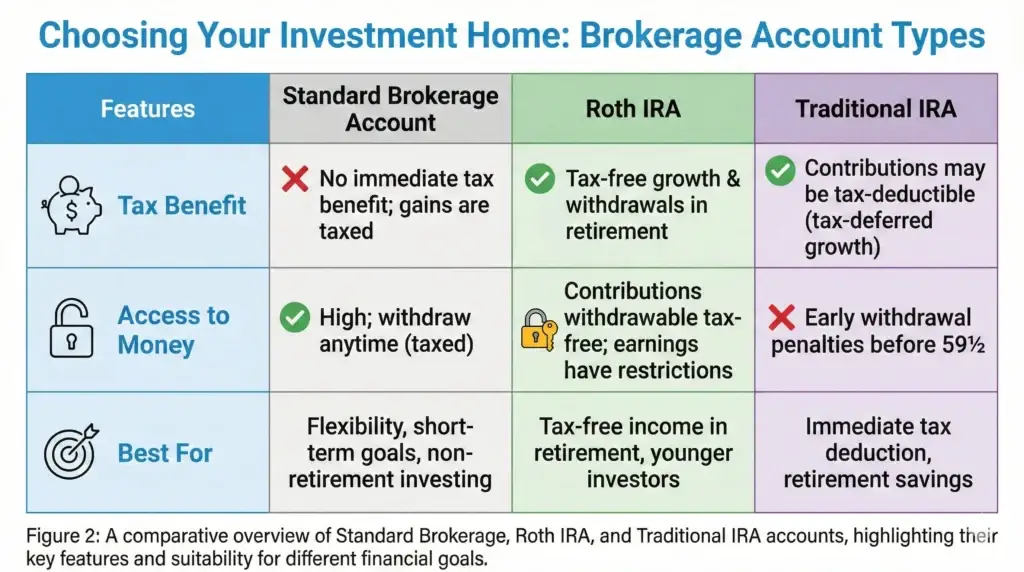

Choosing the right account type determines tax implications and access to funds. Brokerage services provide access to various investment products. Popular platforms include Fidelity, Vanguard, and Charles Schwab. These firms facilitate buying and selling stocks and other securities. Account setup typically involves identity verification and linking a bank account.

Roth IRA vs. Traditional Brokerage

A Roth IRA provides tax-free withdrawals in retirement, funded with after-tax dollars. Contributions are limited annually, often around $7,000 for 2024.

A traditional brokerage account offers immediate access to funds and taxes capital gains, not contributions. These accounts serve different financial objectives and tax strategies.

Consulting a tax professional is crucial for specific advice. We do not provide tax or legal advice.

Ready to Elevate Your Trading?

You have the information. Now, get the platform. Join thousands of successful traders who use Volity for its powerful tools, fast execution, and dedicated support.

Create Your Account in Under 3 MinutesStep 4: Fund Your Account

After opening an account, the next step involves transferring money. Most brokerages accept electronic transfers from bank accounts, typically taking 1-3 business days. Other methods include wire transfers or mailing a check. However, these often incur higher fees or longer processing times. Understanding funding limits and associated fees is important for efficient capital allocation.

| Funding Method | Average Fees | Processing Time |

| Electronic Bank Transfer (ACH) | $0 | 1-3 Business Days |

| Wire Transfer | $15-$30 | Same Day to 1 Business Day |

| Check Deposit | $0 | 2-5 Business Days |

Step 5: Pick Your Stock or Fund

Individual stocks from exchanges like NYSE require research into company financials and stock market sectors.

Diversified funds, such as Exchange Traded Funds (ETFs) or mutual funds, hold baskets of stocks, providing immediate diversification. Value investing focuses on undervalued companies, while growth investing targets rapidly expanding firms, both of which require skills to analyze shares effectively.

Step 6: Execute Your First Trade

Executing a trade involves selecting the investment and specifying the order type. A market order buys or sells immediately at the current market price, prioritizing speed.

A limit order sets a specific price an investor is willing to pay or receive, prioritizing price control. Understanding these differences prevents unexpected trade outcomes. Always review order details before confirmation to avoid errors.

Step 7: Review and Rebalance

Investing is an ongoing process. Regularly reviewing the portfolio ensures alignment with financial goals.

Rebalancing involves adjusting asset allocations back to target percentages. For example, if stocks outperform, an investor might sell some stocks and buy bonds.

This maintains the desired risk level. This periodic review helps manage risk and optimize returns over the long term.

Investing Rules and Strategies for Newbies

Effective stock investing extends beyond simply buying and selling. Specific rules and strategies mitigate risk. They also enhance long-term returns for new investors. These methodologies provide a structured approach to market participation. Understanding these concepts helps build a resilient investment portfolio.

The 3-5-7 Rule Explained

The “3-5-7 Rule” in stock investing is a concept discussed in trading communities, referring to specific moving average crossovers. It suggests potential buy or sell signals when the 3-day, 5-day, and 7-day exponential moving averages (EMAs) align or cross.

For instance, a bullish signal occurs when the 3-day EMA crosses above the 5-day and 7-day EMAs. While popular among some traders for short-term decision-making, it carries significant risk.

This risk is due to market noise and whipsaws. This rule applies to technical analysis, which focuses on price charts rather than company fundamentals.

Dollar-Cost Averaging (DCA)

Dollar-Cost Averaging (DCA) is a powerful strategy for beginners. It involves investing a fixed amount of money at regular intervals, regardless of market fluctuations.

For instance, investing $100 every month means buying more shares when prices are low and fewer when prices are high. This averages the purchase price over time, reducing the impact of market volatility. DCA effectively removes the emotional element of market timing.

Why timing the market usually fails for beginners?

Attempting to predict market highs and lows (market timing) rarely succeeds for experienced investors, let alone beginners. Studies consistently show that time in the market outperforms timing the market. Missing just a few of the best-performing days significantly reduces overall returns. DCA provides a disciplined alternative. It ensures consistent participation without the stress of predictions.

Diversification and the “Sleeping Well” Test

Diversification spreads investments across various assets, industries, and geographies. This strategy reduces the impact of poor performance from any single investment.

A diversified portfolio might include a mix of stocks, bonds, and real estate. The “sleeping well” test asks: “Does your investment portfolio allow you to sleep soundly at night?”

If market fluctuations cause undue stress, your portfolio might be overly concentrated or too risky. Adjusting diversification can improve peace of mind.

Realistic Growth: The Math Behind Your Money

Understanding the mathematical principles behind investment growth helps set realistic expectations. This section clarifies how small, consistent contributions accumulate into substantial wealth over time. It also debunks common misconceptions about rapid returns. Real wealth building prioritizes patience and compound interest.

The Power of Compound Interest

Compound interest represents interest earned on both the initial principal and the accumulated interest from previous periods. This “interest on interest” effect dramatically accelerates wealth growth.

For example, $100 invested monthly for 30 years at a 7% average annual return grows to approximately $122,700. If the average return increases to 10%, that same $100 monthly investment yields about $201,300 over 30 years. This demonstrates the significant impact of consistent contributions and time.

📌 REMEMBER: Compound interest is the most powerful force in investing. Even small, regular contributions can grow into substantial wealth over decades.

Managing Expectations

Financial forums often showcase unrealistic expectations. These include turning minimal capital into fortunes rapidly. Genuine investing focuses on consistent, sustainable growth. A realistic annual return for a diversified stock portfolio historically averages 7-10%. Achieving this requires patience and adherence to a long-term strategy.

Why “Turning $1000 into $10000 in a month” is gambling, not investing?

High-risk strategies, such as aggressive options trading or speculative penny stocks, offer the allure of quick profits. However, these methods significantly increase the risk of substantial losses.

Transforming $1,000 into $10,000 within a month would require a 900% return. This scenario is typically associated with gambling, not a sound investment strategy. These activities often involve leverage, magnifying both gains and losses.

Realistic timelines for doubling your money (Rule of 72)

The Rule of 72 provides a quick estimate for how long it takes an investment to double. Dividing 72 by the annual rate of return gives the approximate number of years. For an average market return of 7%, money doubles every 10.3 years (72 / 7 = 10.28). At a 10% return, money doubles every 7.2 years (72 / 10 = 7.2). This framework helps set achievable growth timelines.

Turn Knowledge into Profit

You've done the reading, now it's time to act. The best way to learn is by doing. Open a free, no-risk demo account and practice your strategy with virtual funds today.

Open a Free Demo AccountComparison: Account Types for Beginners

Selecting the appropriate investment account is a foundational decision. Each account type offers distinct advantages related to taxes, access to funds, and suitability for various financial goals. Understanding these differences empowers beginners to choose wisely, potentially with guidance from a financial planning expert.

Standard Brokerage Account: This account is highly flexible. It allows investors to access their money at any time without penalty. Gains on investments are taxed annually or upon sale. These accounts suit short-to-medium-term financial goals. Examples include saving for a home down payment.

Roth IRA: A Roth IRA is designed for long-term retirement savings. Contributions are made with after-tax money. This means qualified withdrawals in retirement are entirely tax-free. It provides powerful tax advantages for those expecting to be in a higher tax bracket later in life.

Traditional IRA: A Traditional IRA offers tax-deductible contributions in the present. This reduces current taxable income. Withdrawals in retirement are taxed as ordinary income. It suits individuals who expect to be in a lower tax bracket during retirement. Both IRAs have strict withdrawal rules before age 59½.

Key Takeaways

- Start investing early, even with small amounts like $100, to leverage compound interest.

- Understand that fractional shares make high-priced stocks accessible to beginners.

- Prioritize defining clear financial goals before choosing investment vehicles.

- Utilize Dollar-Cost Averaging to mitigate market volatility and eliminate timing stress.

- Diversify your portfolio to manage risk and align with your personal risk tolerance.

Bottom Line

Moving from initial interest to actively investing in stocks demands a systematic approach. The process begins with understanding that small, consistent capital can achieve significant growth through mechanisms like fractional shares and compound interest. The critical path involves defining financial goals, selecting an appropriate brokerage account, and consistently funding it. This is all while embracing disciplined strategies like Dollar-Cost Averaging. Prioritizing long-term wealth building over speculative gains protects capital. Begin with a clear strategy, adhere to consistent contributions, and continuously educate yourself to navigate the market effectively.

FAQ

References

- Investor.gov – Investing Basics

- SIPC – About SIPC

- FINRA – Savings & Investing

- Fidelity – Investing for Beginners

- Investopedia – Rule of 72