Investing in financial products involves risk. Losses may exceed the value of your original investment.

Bitcoin etf outflows is a core topic for traders in 2026. The complete guide follows.

Crypto markets bleed as Bitcoin ETFs hit fifth day of outflows

Crypto had the feel of a crowded theatre when someone shouts “fire”. Not everyone ran. However, enough did to make prices lurch.

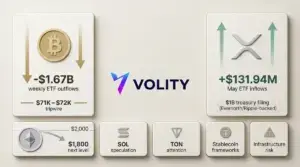

US-listed spot Bitcoin ETFs saw another $103.5 million of net outflows on Friday. Therefore, the run has stretched to five straight sessions of redemptions.

Since 16 January, roughly $1.72 billion has left the group. Meanwhile, BlackRock’s iShares Bitcoin Trust (IBIT) carried most of Friday’s damage, with $101.62 million redeemed. Fidelity’s Wise Origin Bitcoin Fund (FBTC) lost $1.95 million.

Total assets under management across the spot Bitcoin ETF complex fell to about $115.88 billion. That matters because the ETF wrapper has been crypto’s easiest on-ramp for institutions. When the ETF tide goes out, the rest of the market feels colder.

Bitcoin slipped below $90,000 and traded around $89,555, down about 0.52%. Meanwhile, traders pointed to hedge funds unwinding basis trades as yields compressed towards Treasury-like levels. When that spread shrinks, the “safe” carry starts to look like work.

Ethereum products did not get a pass. Spot Ethereum ETFs logged $41.74 million of outflows, extending a four-day run that totals roughly $611 million. Therefore, the market’s message looks simple: the big wrappers are not absorbing risk right now.

Etfs multiply amid the chaos

Yet the oddity of crypto is that the plumbing gets built fastest during the leaks. Institutions are not abandoning the space. Instead, they are changing the kind of exposure they want.

21Shares launched what it called the first Dogecoin spot ETF in the US, listed on Nasdaq. Meanwhile, ARK Invest filed for CoinDesk 20 Crypto Index ETFs. Grayscale submitted an S-1 for a BNB ETF, and Bitwise rolled out a Bitcoin-gold active ETF.

Elsewhere, tokenisation continued its slow march from concept to habit. Ondo Finance tokenised BitGo stock after BitGo’s $212.8 million IPO filing, led by CZ-backed YZi Labs.

- European banks formed a consortium for a euro-pegged stablecoin, a sign of TradFi’s steady crypto push.

- UBS weighed a Bitcoin and Ethereum trading desk entry, while Senate Republicans advanced a market bill despite travel disruption from snow.

- In Washington, talk grew of a more unified SEC-CFTC stance under a Trump era policy reset.

Solana shines with network surge and bullish forecasts

While Bitcoin wobbled, Solana kept flashing the sort of utilisation metrics that speculators like to screenshot. Network fees, transactions and user activity rose. Therefore, the pitch is back: Solana could outpace Ethereum on “activity” in the first quarter.

Some analysts set a near-term marker of $142 by late February, about 12% up from recent levels. Longer-range forecasts for 2026 ranged from $127 to $289 in bullish cases, while other models quoted €114 to €127.

Changelly put an average 2026 price near $201, while Binance projections stretched to $207 by spring. Meanwhile, the “top buys” lists rotated again, with names like BlockDAG and Hyperliquid joining SOL and ETH in trader chatter.

Nfts rebound, vc flows strong, but risks loom

Risk appetite did not vanish. It just reappeared in stranger corners.

NFT sales jumped 101% to $122.5 million, with CryptoPunks up 25%. Meanwhile, venture funding headlines stayed lively. BitGo’s $212.8 million IPO filing drew attention, while Superstate raised $82.5 million.

Market structure, though, still looks fragile. XRP threw off uneasy chart signals as funding rates flipped negative, even as Ripple executives talked up the longer game. Altcoins held at roughly $1.3 trillion in aggregate, while BNB stayed resilient despite the prospect of a Grayscale-linked ETF wrapper.

Wild cards: hacks, politics, and miners

Then come the wild cards, the ones that do not show up in a neat valuation model.

South Korea reported $48 million in seized Bitcoin lost to phishing. France’s Waltio faced a ransom demand from hackers. Meanwhile, Tennessee advanced zoning rules for crypto mining.

Mining competition also turned sharper. Bitdeer edged ahead of Marathon Digital (MARA) on hashrate while talking up an AI pivot. Therefore, miners are again selling a story that is not purely Bitcoin.

Politics kept injecting volatility. Trump sued JPMorgan for $5 billion over alleged “debanking”. His Greenland comments whipsawed risk sentiment, and policy uncertainty sat behind soft moves in Pi, XRP and ETH.

An options expiry of roughly $2.3 billion in BTC and ETH sat on the calendar, a reminder that forced positioning can arrive on schedule even when the news does not.

By the numbers

- Spot Bitcoin ETF flow (Friday): -$103.5m

- Cumulative outflows since 16 January: -$1.72bn

- IBIT flow (Friday): -$101.62m

- Spot Ethereum ETF flow (Friday): -$41.74m

- Bitcoin price: about $89,555

Key takeaways

- ETF outflows keep pressure on BTC’s spot bid, so rallies may struggle without a flow reversal.

- Basis-trade unwinds can accelerate downside when spreads compress, especially into options events.

- Solana’s activity surge is a tailwind, although it can turn quickly if fee spikes deter users.

- NFT and VC pockets look lively, yet they often behave like late-cycle risk gauges.

- Watch policy headlines and security incidents, because they can overwhelm fundamentals fast.

For more on this topic see our deep-dives on Bitcoin Highs and Regulatory Crackdowns: An Investor Framework, Bitcoin, Geopolitics and the FOMC: How Headline Risk Triggers Liquidations, and Bitcoin Price Surges and Crypto Market Cap Climbs: What Drives Rallies.

By Alexander Bennett, Volity markets desk

What our analysts watch: Three reads convert daily outflow prints into a multi-week thesis. Cohort outflow concentration (the share of total outflow concentrated in the top one to two issuers; concentration above 70 percent argues issuer-specific story, concentration below 50 percent argues macro story). Outflow versus realised price action divergence (sustained outflow during a flat or rising spot tape signals capacity to absorb the redemption flow without price impact, which is constructive; outflow combined with falling spot signals demand exhaustion, which is the structural-warning read). Rolling four-week net flow trajectory (a single week of outflow inside a positive trailing-four-week trend is statistically noise; three consecutive weeks of outflow is a regime indicator that warrants tighter sizing). Reading the three together, the allocator distinguishes tactical noise from structural shift.

Frequently asked questions

What does a billion-dollar weekly outflow week reveal about the institutional buyer base?

It reveals that the marginal allocator at the prevailing price level has lower conviction than the marginal allocator at the prior week, which is the mechanical definition of demand exhaustion at that level. The price impact of the outflow depends on whether the implied selling pressure clears through the spot market or recycles into other Bitcoin venues; the historical pattern is that roughly 60 percent of ETF redemption flow recycles into direct holdings or alternative wrappers, with the residual 40 percent producing the realised spot price impact. The structural read is that a single billion-dollar week is informative but not regime-defining; three consecutive weeks shifts the read to regime-level. The CoinDesk ETF flow coverage publishes the daily print that anchors the analysis.

How does the macro calendar interact with ETF outflow interpretation?

The interaction is structural rather than incidental. Outflow that concentrates in a Federal Reserve event week carries more macro-driven weight and less Bitcoin-specific weight; outflow that prints during a quiet macro week carries more idiosyncratic weight. The interpretive discipline is to overlay the FOMC calendar, the major options expiry calendar, and the cross-asset volatility regime against the daily flow prints; outflow that aligns with a stress-week elsewhere is more likely to be a portfolio rebalance than a Bitcoin sentiment shift. The Bank of England monetary policy page publishes the calendar that anchors the macro overlay.

Why does issuer-by-issuer flow split matter more than aggregate flow?

Because the issuer-specific drivers (fee tier, secondary-market liquidity, registered investment adviser distribution agreements, in-kind versus cash creation differences) carry different decay profiles than category-wide drivers. A flow split that shows one issuer leaking AUM while peers retain assets typically reflects an authorised participant or large-allocator switch rather than a Bitcoin sentiment change, which is the constructive interpretation that does not require thesis revision. A coordinated flow shift across all issuers is the rarer event that does require thesis revision. The SEC ETF disclosure framework covers the underlying disclosure architecture.

Should retail allocators time entries against ETF outflow prints?

The framing that survives the cycle is to use outflow prints as a sizing input rather than a timing input. A multi-week outflow sequence argues for tighter incremental sizing on the next dollar-cost-average tranche; it does not argue for liquidating an existing position or for trying to call the bottom. The historical hit-rate of retail attempts to time the outflow-to-inflow inflection is materially below the hit-rate of disciplined dollar-cost-average frameworks that simply slow the pace during outflow weeks. The structural framing is sizing first, timing second.

Related guides

- Bitcoin explained

- Ethereum explained

- Cryptocurrency trading

- Crypto trading platforms

- Best crypto investments

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.