Investing in financial products involves risk. Losses may exceed the value of your original investment.

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.

Quick answer

Leveraged crypto trading uses borrowed capital to amplify position size on cryptocurrency price movements. EU retail leverage on crypto CFDs is capped at 1:2 with mandatory negative balance protection. Offshore exchanges offer 50x to 125x leverage but expose traders to liquidation cascades, funding-rate drag, and counterparty risk. Most retail leveraged crypto traders blow up within 90 days.

Leveraged crypto trading is borrowing exposure against a smaller cash deposit, multiplying both potential profit and potential loss. At 1:2 leverage, a 1% move in BTC produces a 2% move in your equity. At 1:10 (offshore venues, professional clients), a 10% move wipes the position. Crypto is roughly three to five times more volatile than major FX pairs, which is why ESMA caps retail crypto leverage at 1:2 in the EEA. The math is unforgiving and the failure modes are predictable. This article walks through both, with the regulatory floor and the practical pitfalls.

The ESMA leverage caps

Under ESMA product-intervention measures, made permanent by national competent authorities including CySEC, retail clients in the EEA face the following caps:

| Asset class | Retail leverage cap |

|---|---|

| Major currency pairs | 1:30 |

| Non-major currencies, gold, major indices | 1:20 |

| Other commodities, non-major indices | 1:10 |

| Individual equities | 1:5 |

| Cryptoassets | 1:2 |

The crypto cap is the lowest because crypto realised volatility is the highest. Annualised realised volatility on BTC has ranged from roughly 40% to 90% over the past five years; on EUR/USD, 6-8%. The cap is calibrated to roughly equalise risk-of-ruin per unit of margin across asset classes.

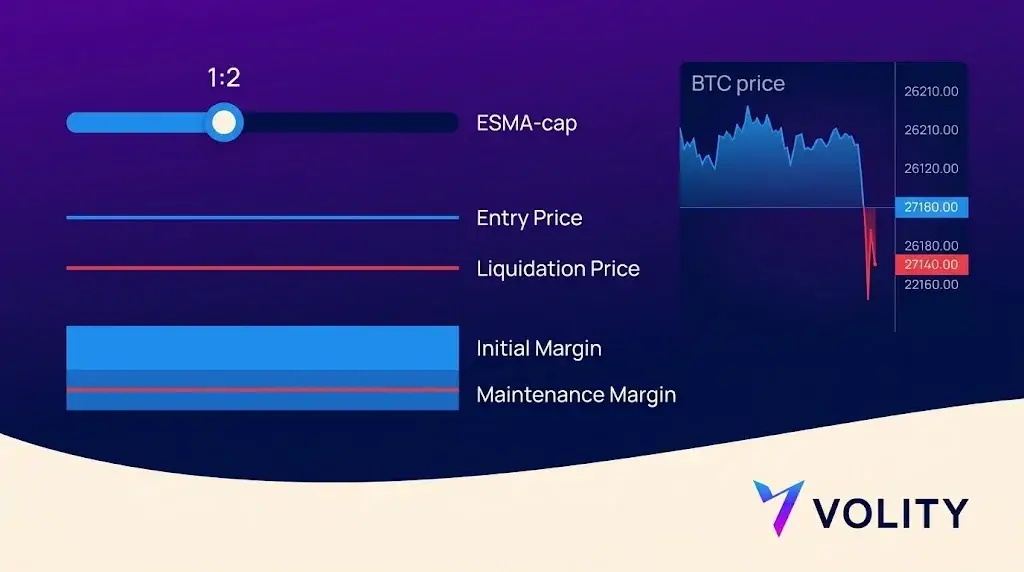

The three margin numbers that run a leveraged trade

- Initial margin: deposit required to open. At 1:2, this is 50% of notional.

- Maintenance margin: minimum equity to keep the position open. Below this triggers a margin call.

- Liquidation price: the level at which the broker auto-closes the position to prevent further loss.

Liquidation math, worked example

You long 1 BTC at $60,000 with 1:2 leverage. Initial margin: $30,000. Suppose maintenance margin is 25% of notional, or $15,000.

- Equity at entry: $30,000.

- Price drops to $50,000. Position is down $10,000. Equity: $20,000. Above maintenance, no call.

- Price drops to $45,000. Position down $15,000. Equity: $15,000. At maintenance; margin call.

- Price drops to $40,000 before you can react. Equity: $10,000. Below maintenance; broker liquidates.

Negative balance protection on EEA retail accounts means you cannot owe more than the initial $30,000 margin posted. Your worst-case loss is the deposit, not unbounded.

Why higher offshore leverage is a trap

Some offshore venues offer 1:50, 1:100, or even 1:125 leverage on crypto. The math:

- At 1:100, a 1% adverse move wipes the position.

- BTC has had multiple 5%+ daily moves per year for the entire history of the asset.

- Probability of a 1% move within an hour is high. Probability within a day is near 100%.

Result: leveraged retail accounts at offshore venues are essentially structured to liquidate. The long-run survival rate at 1:100 is statistically near zero. The CFTC and ESMA have published multiple warnings on this. The 1:2 EEA cap is the regulator’s recognition of the math.

The four classic failure modes

- Leverage creep. Starting at the cap and being satisfied; then opening multiple positions cross-margined to amplify effective leverage; then chasing losses at higher size. The risk-of-ruin curve is non-linear.

- Funding ignorance on perpetuals. Holding a leveraged perp for weeks without modelling the 8-hourly funding cost. A 0.05% per 8h rate is roughly 54% annualised; on a 1:2 levered position, that is 108% on equity. A profitable thesis can be erased by carry alone.

- Stop-loss complacency. Stops on crypto can fail to fill at the advertised price during news gaps. Weekend liquidity is 30-50% of weekday volume. A 10% gap on a Sunday opening is not unusual.

- Position-sizing failure. Risking 5-10% of equity per trade. A 5-trade losing streak (statistically common) cuts the account by 40%. A 10-trade streak cuts it by 65%. Risk per trade should be 0.5-1% of equity, full stop.

The right way to use 1:2

Leverage is a precision tool, not a multiplier of conviction. Three uses we see consistently from disciplined retail flow:

- Capital efficiency on hedges. Pairing a long-term spot bag with a short perp at 1:2 to cut downside while preserving the underlying.

- Tactical short exposure. Spot is long-only. Leveraged contracts allow expressing bearish views.

- Position-sizing flexibility. A 1:2 position lets you size a trade against a structural stop while keeping the cash buffer needed to take the next trade without forced selling.

Stress windows worth remembering

- March 2020 COVID crash. BTC fell 50% in 48 hours. Retail leveraged accounts were almost entirely liquidated.

- May 2021 deleveraging. BTC fell from $58,000 to $30,000 in 9 days. Open interest in perpetuals dropped 60%, mostly via liquidations.

- November 2022 FTX collapse. BTC fell 25% in a week amid contagion fears; cross-margined accounts on FTX were unrecoverable.

Leveraged crypto at Volity

Volity offers crypto CFD exposure on 20+ coins. Retail leverage is capped at 1:2 on cryptoassets under ESMA product-intervention measures. Negative balance protection applies on retail accounts. Execution is by UBK Markets Ltd, a Cyprus Investment Firm authorised by CySEC under licence 186/12. Eligible retail clients are covered by the Cyprus Investor Compensation Fund up to EUR 20,000 per client per firm. Professional clients on request, classified under MiFID II Annex II criteria, can access higher leverage subject to a suitability assessment.