Markets Wait on the Fed, Chips and Policy Risk

Wall Street has three clocks running today. One sits in Washington, one in Taiwan, and one in every energy ministry.

The first measures the Federal Reserve’s patience. The second tracks the supply of advanced chips. The third counts the cost of climate policy, tariffs and power shortages.

Together, they explain why the tape feels jumpy. Stocks still want lower rates. Tech still wants more computing capacity. Energy buyers, meanwhile, want rules they can actually model.

Fed Watch is Still the Main Trade

The Fed remains the market’s metronome, even when it says little. Traders want rate cuts, but inflation has not fully obeyed.

Headline inflation has cooled from its post-pandemic peak. However, the Fed’s 2% target still matters most in core services, wages and shelter.

That leaves investors stuck between two trades. A soft landing helps equities and credit. A sticky inflation print lifts yields and punishes long-duration growth shares.

Therefore, the monthly inflation report now carries the weight of an earnings season. One strong rent line can move the Nasdaq 100. One weak wage print can flatten the dollar.

The labour market tells a similar half-story. Unemployment remains low by historical standards. Yet job openings have fallen, hiring has slowed, and some employers sound more careful.

For traders, the exact first cut date matters less than the path of real yields. If inflation falls faster than nominal Treasury yields, financial conditions ease. If not, risk assets wobble.

- Watch the two-year Treasury: it is the cleanest read on Fed expectations.

- Watch the 10-year Treasury: it drives housing, equity multiples and global discount rates.

- Watch the dollar index: it shows whether higher-for-longer is biting abroad.

Still, the danger lies in crowding. Rate-cut hopes can build quietly, then disappear in one morning. Options traders know that rhythm too well.

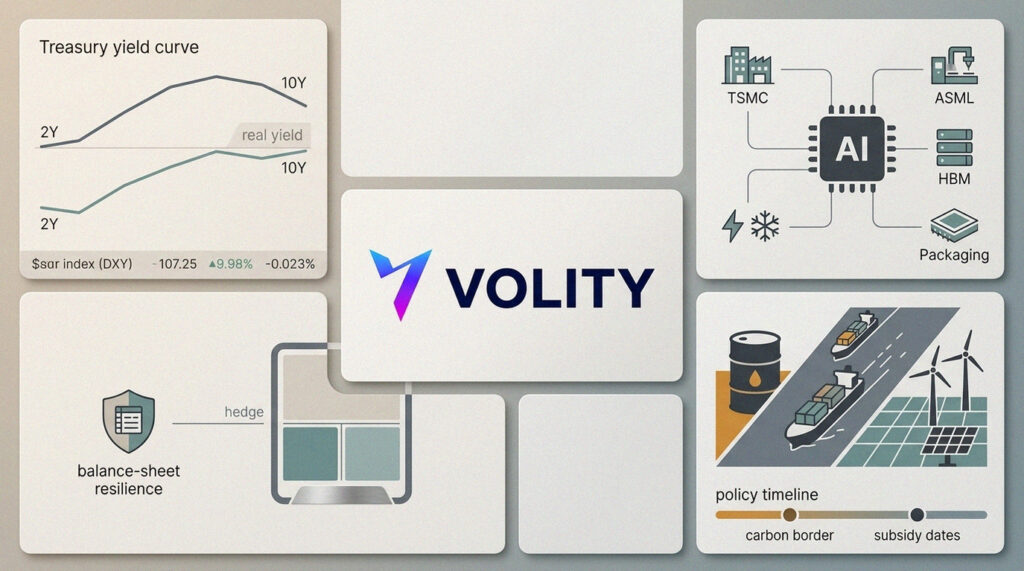

Ai Chips Move from Boom to Constraint

Meanwhile, the technology trade has narrowed into something physical: chips, packaging, power and cooling.

Artificial intelligence may sound weightless. However, the business depends on factories, wafers, high-bandwidth memory and data centres that drink electricity.

Nvidia, ticker NVDA, remains the market’s shorthand for the boom. AMD, ticker AMD, wants a larger slice. Broadcom, ticker AVGO, sits closer to custom silicon and networking.

Yet the supply chain starts much further back. Taiwan Semiconductor Manufacturing, ticker TSM, controls critical advanced foundry capacity. ASML, ticker ASML, sells the extreme ultraviolet machines that make the most advanced chips possible.

Memory matters too. Micron, ticker MU, and SK Hynix have benefited from demand for high-bandwidth memory. Without it, expensive processors wait around like sports cars without tyres.

Cloud spending is the next tell. Microsoft, Amazon and Alphabet are spending heavily on AI clusters. Their capital expenditure plans now shape the earnings outlook for half the semiconductor complex.

However, investors should separate demand from digestion. Companies can order too much hardware. Customers can delay software spending. Margins can peak before revenue does.

The old semiconductor cycle has not vanished. It has put on a more expensive suit.

Related coverage on Volity

- AI Earnings Test: Adobe (ADBE) and Oracle (ORCL) in Focus

- Bitcoin Price Wobbles as Tokenisation Goes Mainstream

- Today Stock Market Watchlist: CASY, AAOI, DKNG, SPY, QQQ

- Bitcoin Price Slips Below $61k as ETF Outflows Hit Crypto

- Oracle (ORCL) Earnings: Key Stocks to Watch Pre-Market

By the Numbers

- 2%: the Fed’s inflation target, still the anchor for bond pricing.

- NVDA: the stock many investors use as the AI risk barometer.

- 2026: the year the EU carbon border charge is set to start collecting payments.

- $7,500: the headline US consumer EV tax credit, subject to eligibility rules.

- OPEC-plus: the producer group still capable of changing oil sentiment overnight.

Energy Policy Becomes a Volatility Machine

The third market driver looks less glamorous, but it may be more awkward. Energy prices increasingly move on policy as much as supply.

Oil traders still watch inventories, refinery runs and OPEC-plus decisions. However, they must also watch sanctions, election promises and shipping risk.

Natural gas adds another layer. A mild winter can crush prices. A hot summer can revive them. Meanwhile, power grids face growing demand from data centres and electrification.

Green energy stocks have suffered a different problem. Falling technology costs should help demand. Higher rates, slow permits and shifting subsidies have often hurt equity holders.

Solar manufacturers face tariff fights and inventory gluts. Wind developers face financing costs, local opposition and vessel shortages. Battery makers face volatile lithium prices.

Therefore, the transition trade has become less about slogans and more about spreadsheets. Cash flow, grid access and subsidy quality now matter more than installed-capacity headlines.

The EU’s carbon border policy is a good example. Importers of steel, cement, aluminium and fertilisers must prepare for carbon-related costs. Those charges can change sourcing decisions.

In the United States, the Inflation Reduction Act still supports batteries, hydrogen, carbon capture and electric vehicles. However, election risk keeps investors cautious.

What This Means for Portfolios

These three stories do not sit in separate boxes. They collide in the same trades.

Higher real rates hit speculative tech and renewable developers first. Strong AI spending supports chip stocks, but it also strains power markets. Energy policy can lift industrial costs and inflation expectations.

So the market’s best-looking trade can carry hidden baggage. A semiconductor winner may depend on utility capacity. A green manufacturer may depend on a tax credit. A bank may depend on deposit costs and the yield curve.

For equity investors, balance sheets deserve more attention. Companies with near-term refinancing needs look exposed if yields refuse to fall. Those with pricing power can wait longer.

For bond investors, duration is still a live weapon. It can help when growth slows. However, it hurts quickly when inflation surprises higher.

Currency traders should keep the dollar near the centre of the map. A firm dollar tightens conditions for emerging markets. It also squeezes companies with foreign revenues.

Trading Checklist

- Start with rates. Compare the two-year yield, 10-year yield and inflation expectations before chasing equity moves.

- Read tech vertically. Follow ASML, TSM, MU, NVDA and cloud capex guidance, not just glossy product launches.

- Map policy dates. Track elections, tariff reviews, carbon rules and subsidy deadlines as real market events.

- Stress-test winners. Ask what happens if AI demand pauses, rates stay high or power costs rise.

- Keep hedges simple. Index futures, sector ETFs and listed options beat complicated trades during data weeks.

The market does not need a crisis to become difficult. It only needs three big forces pulling at once.

That is where we are now. The Fed sets the discount rate. Chipmakers set the growth mood. Policymakers set the energy bill.

Traders who connect those dots will have an edge. Everyone else will keep blaming the last headline.