Investing in financial products involves risk. Losses may exceed the value of your original investment.

The Crypto Trading Starter Kit

A plain-English PDF: what to check before you trade, how orders and risk really work, and the mistakes to skip. Get it free.

Quick answer

Crypto CFD trading is leveraged speculation on cryptocurrency price without holding the actual coins or their custody risk. EU retail leverage is capped at 1:2 with mandatory negative balance protection. Crypto CFDs win when the trader wants short exposure, capital efficiency, or to avoid wallet management; spot wins for long-term holding, on-chain use, or self-custody.

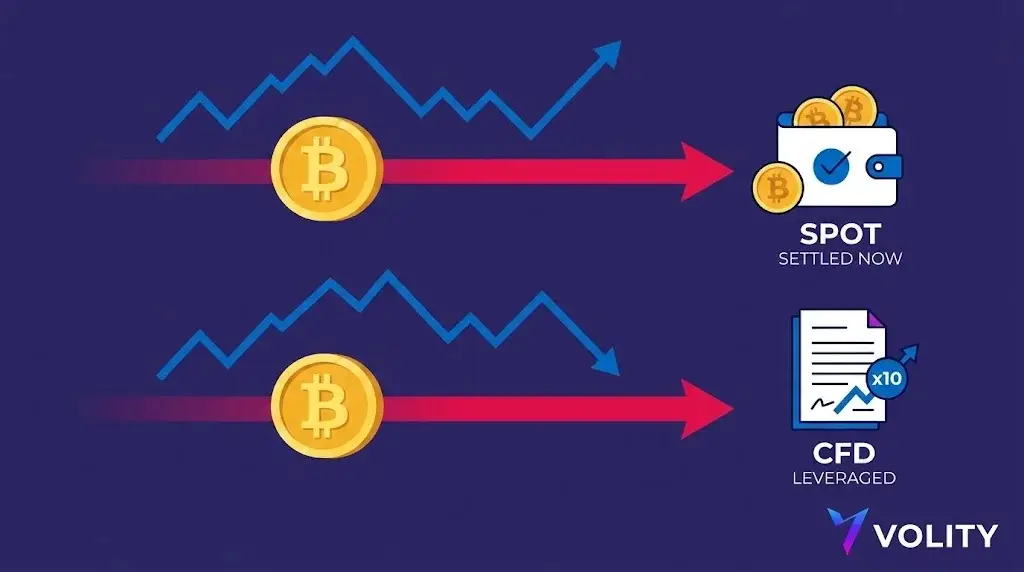

A crypto CFD is a contract that pays the difference between the entry price of a coin and the exit price, settled in cash. You never hold the underlying token. A spot trade is the opposite: you pay the live price and own the asset until you sell it. Both are legitimate ways to express a crypto view. Which one wins depends on your time horizon, whether you need to short, and how you want to handle custody and tax.

How does crypto CFD trading work?

You post margin. The platform tracks the underlying price. Your equity moves on the full notional. You can go long or short. There is no token in your wallet, no on-chain confirmation, no withdrawal address. The position lives until you close it (or, on a futures-style contract, until expiry). Leverage on retail crypto CFDs in the EEA is capped at 1:2 under ESMA product-intervention measures.

How does spot trading work?

You buy the underlying coin at the live ask. Settlement is near-instant on most platforms. The asset sits in custody (broker or self-custodied wallet). You can hold indefinitely, transfer on-chain, or sell at any future price. There is no leverage on a pure spot trade and no expiry.

Side-by-side

| Dimension | Crypto CFD | Spot |

|---|---|---|

| Ownership of token | No | Yes |

| Leverage | Up to 1:2 retail (EEA / ESMA) | None |

| Direction | Long or short | Long only |

| Expiry | None on perpetual-style; fixed on dated futures | None |

| Custody risk | Broker contract; no on-chain risk to user | User-held or exchange-held; on-chain risk applies |

| Funding / overnight cost | Yes, daily financing on borrowed portion | No |

| Negative balance protection | Yes (retail) | N/A |

| Withdrawal of underlying | No | Yes |

| Tax treatment | Often treated as derivative; jurisdiction-dependent | Capital gains on disposal; jurisdiction-dependent |

When does CFD win?

- Short directional bias. CFDs let you short. Spot does not.

- Capital efficiency on a multi-asset book. 1:2 leverage on a $10,000 BTC position uses $5,000 of margin, freeing the rest for other positions.

- Hedging an existing spot stack. Short a CFD against your long-term holdings to neutralise short-term downside without selling.

- Single account, multi-asset. CFD platforms put crypto, FX, indices, and commodities on one rail. One KYC, one statement, one withdrawal queue.

When does spot win?

- Long-horizon conviction. If your view is two years out, spot has no carry. CFD has daily financing.

- You want the token. Staking, on-chain governance, transferring to self-custody. Spot is the only path.

- Tax simplicity in some jurisdictions. Long-held spot can qualify for preferential capital-gains treatment that derivative trades do not.

- You are early in the learning curve. No leverage, no liquidation, no funding. Spot lets you focus on entry, exit, and sizing without the lever.

What does each cost?

- CFD: spread + daily financing on borrowed portion + slippage on fast moves.

- Spot: spread + commission (sometimes) + on-chain network fee on withdrawal.

For a 24-72 hour trade, CFD financing is small enough to be noise. For a 6-month hold, financing compounds and starts to bite; spot is usually the cleaner expression.

What goes wrong

- Using CFDs for long-term conviction. Daily financing eats the position. Wrong tool.

- Using spot for tactical shorting. You cannot. Wrong tool.

- Self-custody errors on spot. Lost seed phrases, phishing attacks. The user owns the operational risk.

- Leverage creep on CFDs. Starting at 1:2 nominal, then sizing as if it were 1:5. The math does not change because of optimism.

Crypto CFD and spot at Volity

Volity offers crypto CFD exposure on 20+ coins on a regulated account. Retail leverage is capped at 1:2 (ESMA). Professional clients on request may access higher leverage subject to a MiFID II suitability assessment. Negative balance protection applies on retail accounts. For the unleveraged definition see our spot trading guide. Execution is by UBK Markets Ltd (CySEC 186/12).

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.