Investing in financial products involves risk. Losses may exceed the value of your original investment.

The Crypto Trading Starter Kit

A plain-English PDF: what to check before you trade, how orders and risk really work, and the mistakes to skip. Get it free.

Quick answer

Crypto arbitrage trading is the simultaneous buying and selling of the same asset on different venues to capture price discrepancies. Common variants: cross-exchange (buy cheap on A, sell rich on B), futures-spot basis arbitrage, and DEX-CEX arbitrage. Margins are typically 0.05% to 0.30% per round-trip. Retail edge has compressed as MEV bots and market makers compete; institutional infrastructure is now the deciding factor.

Crypto arbitrage trading is the practice of buying an asset at one price and simultaneously selling it at a higher price somewhere else, pocketing the difference. In theory it is risk-free. In practice it is a latency, balance-sheet, and execution arms race that has industrialised over the last five years. Retail discretionary arbitrage in liquid majors has effectively zero edge after fees. Where retail can still play: cross-protocol gaps, regional rate-limit arbitrage, and triangular paths in less-liquid altcoins.

The four arbitrage families

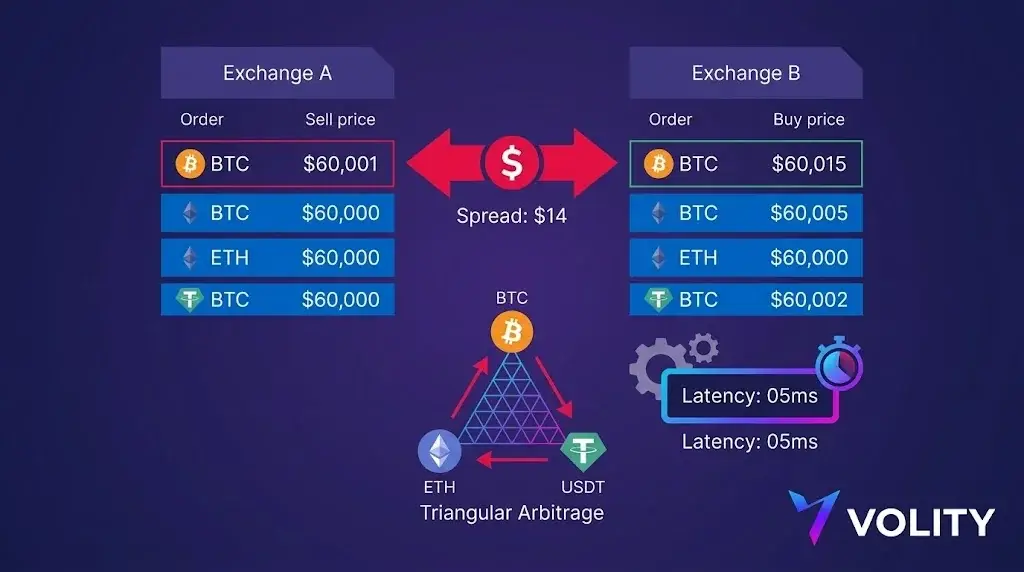

- Cross-exchange (geographical): BTC on Exchange A trades $1 above BTC on Exchange B. Buy on B, sell on A, capture $1.

- Triangular: BTC/USDT, ETH/USDT, ETH/BTC are mispriced relative to each other. Three trades close the loop.

- Cross-protocol (DeFi vs CeFi): an asset trades $5 cheaper on a DEX than on a centralised venue. Profitable while gas + slippage stays under $5.

- Funding rate: spot long + perpetual short. If funding is positive (longs pay shorts), the short collects. Net: cash-and-carry that earns the funding rate, market-neutral on price.

Why the edge has compressed

Three forces have squeezed retail arbitrage to near-zero on liquid majors:

- Co-located market makers. The biggest crypto firms run sub-millisecond latency. By the time a retail trader sees a $1 gap on a price feed, the gap has been arbitraged.

- Fee asymmetry. Retail pays 0.05-0.1% per trade. Institutional pays 0.0-0.02%. A 0.1% gap is profit for the institutional desk and a loss for the retail desk.

- Withdrawal bottlenecks. Cross-exchange arbitrage requires moving capital between venues. Withdrawal queues, ID-verification holds, and on-chain confirmations turn 30-second arbitrage into 30-minute risk exposure.

Where retail can still find edge

Two pockets in our experience:

- Funding rate cash-and-carry. When funding rates spike on a memecoin or a hyped narrative (annualised 30-50%+), the spot-long perp-short pair can earn that funding net of execution. Capital-intensive but mechanical.

- Cross-protocol DeFi. New L2 launches and DEX-CEX listings create temporary mispricings. Edge requires gas-management discipline and a tolerance for smart-contract risk.

The math of a real arbitrage trade

Suppose BTC bid is $60,005 on Venue A and ask is $60,000 on Venue B. Apparent spread $5 per unit, or 8.3 basis points.

- Round-trip taker fee: 10 bp (5 bp each side).

- Withdrawal fee: 0.0001 BTC = $6 at $60,000.

- Latency risk: a 200ms delay could see the gap close 30% of the time.

Net expected: 8.3 bp gross – 10 bp fees – 1 bp withdrawal – 2 bp latency cost = -4.7 bp. Negative expected value. This is why retail discretionary arbitrage on liquid majors is a learning exercise, not a strategy.

What it actually costs to do this professionally

- Capital. $1m+ across multiple venues to capture meaningful basis points.

- Infrastructure. Co-located servers, websocket feeds, custom matching engines. $50k-150k setup, 10-30k/month run rate.

- Headcount. One quant developer plus one ops person, minimum.

- Fee tier. Either VIP discounts (volume-based) or maker rebates. Plain retail fees kill the trade.

Honest framing

If you are reading a guide on crypto arbitrage with the intent of running it as a strategy, the realistic next step is one of three: (1) accept that arbitrage in 2026 is institutional, and pick a different strategy; (2) focus on funding-rate cash-and-carry, which is mechanical and tolerates retail latency; or (3) treat arbitrage as a tool for understanding market microstructure, then apply that understanding to directional strategies. Volity supports cash-and-carry through CFD exposure on perpetuals plus spot reference pricing on the same account.

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.