Investing in financial products involves risk. Losses may exceed the value of your original investment.

Intel share price is a core topic for traders in 2026. The complete guide follows.

Intel’s turnaround bet runs into its own valuation

Intel shares spent this week arguing with themselves. On one side sat a clean momentum trade. On the other sat the ugly arithmetic of a turnaround priced like a triumph.

INTC traded around $64.86 after it snapped a nine session winning streak. Meanwhile, the stock is up about 31.8% since January 2026. That rise has not been pure vibes. However, it has pushed investors into a familiar corner: paying today for execution that still sits in tomorrow’s diary.

Lip-Bu Tan took over in March 2025 with a manufacturing mandate. He also arrived with a reputation for compounding, after his long run at Cadence. Therefore, the market has given Intel something it lacked for years: belief that the factory story might finally land.

Some proof has followed. Intel has talked up 18A progress and a ramp in foundry activity, while a high profile Terafab partnership story has helped reframe Intel as a builder again. Meanwhile, the company’s fourth quarter 2025 print gave bulls their first clean headline beat in a while.

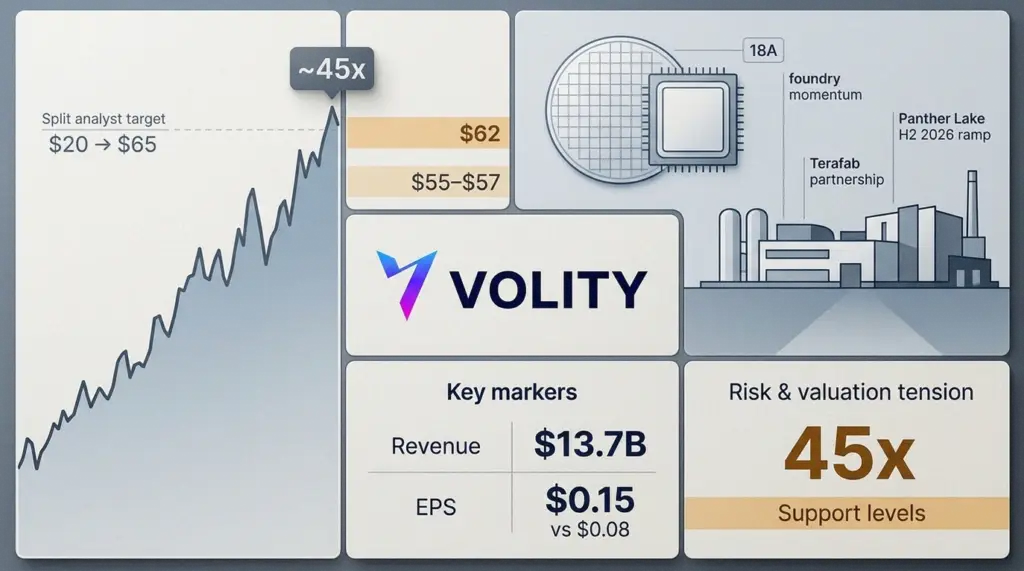

Revenue came in at $13.7 billion and non-GAAP EPS printed at $0.15, above the $0.08 expectation. Those are not numbers that force anyone to rewrite models. However, they do matter in a stock that had started to trade like a stranded asset.

The options tape has matched the renewed confidence. Short put trades around the $64 strike implied a punchy yield, and call activity has stayed heavy on up days. Meanwhile, early week volume spiked, with roughly 12.6 million shares changing hands in the first 15 minutes of one session. That looked like repositioning, not a retail wobble.

Where the story creaks

Valuation has stopped being a footnote. At around 45.5 times earnings on the latest quarter’s run rate, Intel now asks investors to underwrite something close to best case execution. However, forward and “normalised” earnings measures look even more stretched, which is where the discomfort sets in.

Analysts have not lined up behind a single narrative. Consensus sits around Hold, yet published targets run from roughly $20 to $65. Therefore, the debate is not about one quarter’s demand. It is about whether Intel’s manufacturing reboot becomes durable, or just another expensive detour.

The bull checklist is clear. Intel needs Panther Lake to ramp cleanly in the second half of 2026.

It also needs foundry orders to turn into reliable quarterly revenue north of $13.5 billion. Finally, it needs gross margin to lift towards 35% and keep climbing.

Any one miss, however, will look large inside a multiple that already assumes progress.

Momentum traders have a map, but not a safety net

Technicals now show classic late sprint conditions: overbought readings alongside strong trend structure. Therefore, pullbacks can happen fast, even if the longer move remains intact.

The recent slip from about $65.18 to $62 reads like normal digestion after nine green sessions. Meanwhile, the market has started to define a near term line in the sand. Options pricing suggests support thinking sits near $62, while chart watchers keep circling the $55 to $57 zone as the next serious test.

That gap matters because Intel is no longer cheap enough to forgive stumbles. However, it is also no longer broken enough to ignore. The catalyst set is real, yet the stock now charges admission for outcomes, not hopes.

By the numbers

- Last trade area: about $64.86

- Year to date move: roughly +31.8% since January 2026

- Q4 2025 revenue: $13.7bn

- Q4 2025 non-GAAP EPS: $0.15 vs $0.08 expected

- Key levels traders cite: $62 near term, then $55 to $57

Key takeaways

- Momentum is intact, yet the stock now reacts sharply to any execution wobble.

- Options markets imply support around the low $60s, which may anchor dip buying.

- Valuation raises the bar, so “good” updates may not be enough to push shares higher.

- Watch margins, since gross margin recovery is the cleanest fundamental tell.

- Define risk first, because the debate is now about scale delivery, not direction.

Intel has made the turnaround trade tradable again. However, it has also made it expensive. The next leg will not be decided by speeches or partnerships. It will be decided by wafers, yields and margins, quarter after quarter.

For more on this topic see our deep-dives on NVIDIA AI: Blackwell, Autonomous Vehicles and Edge Compute, NVDA Forecast: Predictions, Risks and Where Profits Are Heading, and Sector Rotation Explained: When Energy and Defensives Beat Mega-Tech.

What our analysts watch: Three readings filter narrative from substance on Intel. 18A yield disclosures and external foundry customer wins (Microsoft, AWS, government) tell us whether the foundry strategy is converting from announcements into revenue. Gross margin trajectory (versus the 60% historical baseline) measures how quickly capex absorption is normalising. Federal anchor commitments under CHIPS Act tranches reveal whether the political tailwind is durable or only seasonal. When all three confirm, the rerating to a foundry-multiple becomes credible; when they diverge, the stock trades closer to a margin-pressured legacy CPU multiple.

Frequently asked questions

What is the 18A node and why does it matter?

18A is Intel’s next-generation process node aimed at competing with TSMC’s N2 and Samsung’s SF2. Successful 18A execution converts Intel from a CPU-only chip designer into a credible Western foundry alternative, which is the single highest-leverage element of the turnaround thesis. Yield disclosures and external customer wins are the canonical proof points. Investopedia covers the foundry market mechanics in depth.

How significant is the CHIPS Act for Intel?

The CHIPS and Science Act provides direct grants, loan guarantees, and investment tax credits that materially offset Intel’s domestic capex. The funding is meaningful at the cash-flow level and politically anchors Intel’s domestic build-out, but it does not solve the underlying execution risk. The U.S. Federal Reserve publishes broader industrial policy context that shapes the macro tailwind.

How does Intel compete with NVIDIA in AI?

The Gaudi 3 and Falcon Shores accelerators target the AI training and inference market dominated by NVIDIA’s H100 and B200. Intel’s pricing is more aggressive on a TFLOPS-per-dollar basis, but software ecosystem maturity (CUDA versus oneAPI) remains the decisive factor for most enterprise buyers. The Nasdaq publishes the sector-level revenue and unit economics data that contextualise the comparison.

How should retail investors size an Intel position?

Treat the turnaround as a multi-quarter thesis with binary catalysts (foundry yield, anchor customer wins, CHIPS Act tranches), size positions for the duration mismatch between thesis and price, and avoid concentrating exposure in a single semiconductor name without the underlying basket diversification. Volity research builds semiconductor sector models for clients on its CySEC 186/12 platform.

Related guides

- Best AI stocks to invest in

- How to buy Intel stock

- Stocks investing for beginners

- Best stock trading platforms in Europe

- Best trading platforms

- Risk reward ratio

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.