Investing in financial products involves risk. Losses may exceed the value of your original investment.

Ai stocks rally is a core topic for traders in 2026. The complete guide follows.

Energy shocks bite, yet the AI build-out keeps humming

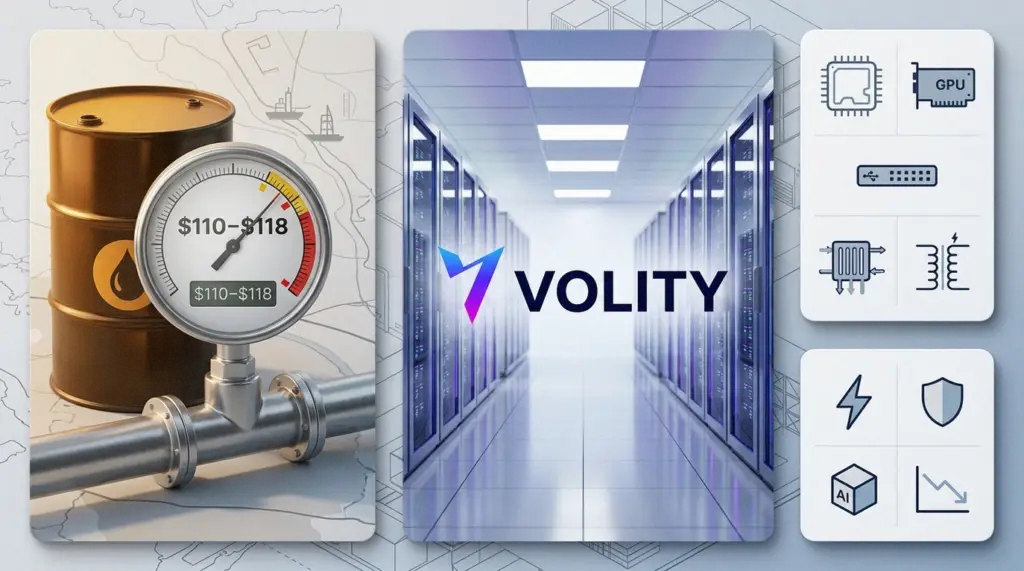

Oil traders woke up again to the same old problem in a new disguise. Geopolitics tightened supply, freight lanes clogged, and refineries priced in disruption. Meanwhile, equity desks treated the energy tape like a hot pan. Crude can rally, but energy shares can still sulk, because costs rise, politics intrudes, and cash flows get discounted harder.

Brent’s jump back towards the $110 to $118 zone has revived an inflationary undertow. However, it has not produced a uniform risk-off dump. Instead, it has sharpened a rotation that traders already felt in their fingertips. Money is drifting away from energy’s operational headaches and towards AI’s concrete spending cycle.

That divergence is the story of 2026 so far. Energy prices are high because supply is brittle. Yet energy equities look less like a clean hedge and more like a governance and logistics argument. By contrast, AI infrastructure looks like visible demand with signed cheques, delivery schedules, and grid connections.

Why energy is lagging, even with higher crude

Energy bulls can point to tight balances and louder headlines. Even so, the sector trades like it is trapped between costs and scrutiny.

Insurance rises when sea lanes look unreliable. Equipment delays bite when supply chains run lean.

Meanwhile, governments talk tough on prices, so the upside feels politically capped.

Therefore, traders have treated many oil sensitive names as a source of volatility, not comfort. The sector’s recent slide, around 4.5% in the period being discussed, fits that mood. Higher oil does not automatically mean higher multiples, especially when inflation threatens demand and raises discount rates.

At the same time, the green transition’s weak plumbing keeps showing. The grid still creaks.

Storage remains patchy. Weather swings strain renewables output.

As a result, the market keeps paying for energy insecurity, but it does not always pay energy shareholders.

AI capex looks like industrial policy with earnings attached

AI has stopped behaving like a sentiment trade and started behaving like an infrastructure cycle. Morgan Stanley’s often-quoted $2.9 trillion data centre build estimate through 2028 may be debated, yet the direction is clear. Hyperscalers are spending, vendors are shipping, and power contracts are getting signed.

Moreover, the capex numbers have become too big to ignore. The $527 billion 2026 hyperscaler capex figure cited in your draft captures the market’s fixation. Traders see the knock-on effects in semiconductors, networking, cooling, electrification, and the REITs that host the boxes.

Still, the tape is selective. Not every chip is an AI chip. Not every software company gets an automatic re-rating. Consequently, the rotation has looked less like “tech up” and more like “AI plumbing up”.

Where traders are crowding, and what they are fading

Flow has favoured liquid leaders and the picks-and-shovels complex. Meanwhile, traders have kept one eye on rates, because long-duration growth still flinches when yields jump. Even so, AI-linked demand has offered a firmer bid than most sectors.

By the numbers

- Brent crude: $110 to $118 discussed as a plausible stress zone in the current setup.

- Energy sector move: roughly -4.5% referenced, despite firmer crude.

- Data centres: $2.9 trillion build estimate through 2028 cited as a market anchor.

- Hyperscaler capex: $527 billion for 2026 used to frame AI infrastructure demand.

- Energy transition bill: $33 trillion by 2035 flagged as the long-run constraint.

On the longs, semis and infrastructure have remained the core expression.

- NVDA, AMD, TSM and the broad basket via SOXX have stayed central, because capex is hitting orders now, not “one day”.

- AMZN remains a bellwether for cloud spend, while ad-tech beta has kept TTD on traders’ screens.

- PLD fits the second-order trade, as data centres, logistics, and power equipment reshape property demand.

- BK reads as a steadier “rates are not exploding” tell, if broader financials hold their footing.

On the hedges and counter-positions, traders have looked for where costs crush margins.

- NXPI often gets treated as “non-AI semis”, so it can lag when the market narrows to winners.

- JKS and parts of solar can suffer when metals, freight, and currency moves squeeze economics.

- ABT sits in a different universe, yet it can still get dragged by services inflation and risk appetite.

Risks: AI is sturdy, not invincible

The AI trade has its own weak points. Power is the obvious choke.

Cyber risk is the quieter one. Model errors remain a business risk, not just a headline.

Therefore, the market has rewarded firms that spend on resilience, monitoring, and control, even during a growth chase.

Also, valuation still matters. If inflation re-accelerates on energy shock, yields can lift, and crowded longs can wobble. That is why traders keep defaulting to liquid vehicles like QQQ and SPY, then expressing views with narrower overlays.

Key takeaways

- High oil is acting more like a macro tax than a clean equity tailwind for energy.

- AI infrastructure remains the rotation’s spine, because capex has become measurable and persistent.

- Dispersion inside semis is rising, so “own the index” matters less than it did.

- Second-order winners include logistics and power-adjacent names, not only GPU leaders.

- Watch rates: the rotation survives if yields stabilise, but it stumbles if inflation forces them higher.

For now, the market is making a blunt argument. Energy feels fragile in a tense world. AI feels like a build programme that boards approve even when geopolitics turns ugly. Traders are rotating accordingly, and they are doing it with remarkable consistency.

For more on this topic see our deep-dives on NVDA Forecast: Predictions, Risks and Where Profits Are Heading, Stocks to Watch: AAPL, SOFI and the Bank Red Flags Investors Track, and Toyota and NVIDIA: Inside the Autonomous-Vehicle AI Partnership.

What our analysts watch, by Alexander Bennett: Three indicators frame the rotation. Hyperscaler capex guidance tells us whether the AI build cycle still has 18 months of visibility or is starting to wobble.

Real yields and the dollar set the discount rate that hits long-duration AI multiples first. And the energy share underperformance versus crude flags whether the market still believes oil profits convert into shareholder cash.

When capex stays firm and yields stabilise, the AI-plumbing trade tends to widen rather than narrow.

Frequently asked questions

Why are energy stocks lagging when oil prices are this high?

High crude does not automatically translate into higher energy multiples. Insurance premiums rise with shipping risk, equipment delays inflate capex, and political pressure caps perceived upside on margins.

Higher oil also feeds inflation expectations, which lifts the discount rate applied to future cash flows. The U.S.Energy Information Administration tracks the supply, demand, and inventory data that energy desks watch first.

What is hyperscaler AI capex and why does it matter for traders?

Hyperscaler capex is the spending by Amazon, Microsoft, Google, and Meta on data centres, GPUs, networking, and power. The widely cited 2026 figure near $527bn turns AI from a sentiment trade into an industrial cycle with measurable demand. Vendors and power-adjacent REITs benefit second. The Nasdaq publishes sector breakdowns and capex tracking that help size positions in semis, networking, and cooling names.

How should I position around oil-shock risk in 2026?

Position around oil shocks with rules, not opinions. Cap energy exposure at a defined percentage of the book, hedge inflation-sensitive longs with short-duration or quality names, and watch the freight and refinery spread, not just the headline crude price. The International Monetary Fund publishes commodity outlooks that help separate cyclical demand from supply-shock pricing.

Is the AI rally a bubble or an industrial cycle?

It looks more like an industrial cycle today. The capex is signed, the power contracts are dated, and the GPU order books extend by quarters rather than weeks. That said, dispersion inside semis is rising, so owning the index is not the same as owning the winners. At Volity, regulated by CySEC under licence 186/12 via UBK Markets, we treat single-name AI exposure as a position-sized allocation, not a bet-the-portfolio call.

Related guides

- Best AI stocks to invest in

- Stocks investing for beginners

- Indices trading platforms

- Best stock trading platforms in Europe

- Best trading platforms

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.