Forex orders are execution instructions, not guarantees of fill prices or settlement. Market orders during high-volatility sessions can produce significant slippage when the ask-bid spread widens dramatically. Pending orders (stop and limit) may never execute if prices gap past those levels without touching them. The 2026 push toward T+1 settlement introduces new counterparty risk windows. Leverage amplifies losses on poorly-configured orders (missing stop-loss or oversized position). Capital at risk in all leveraged trading.

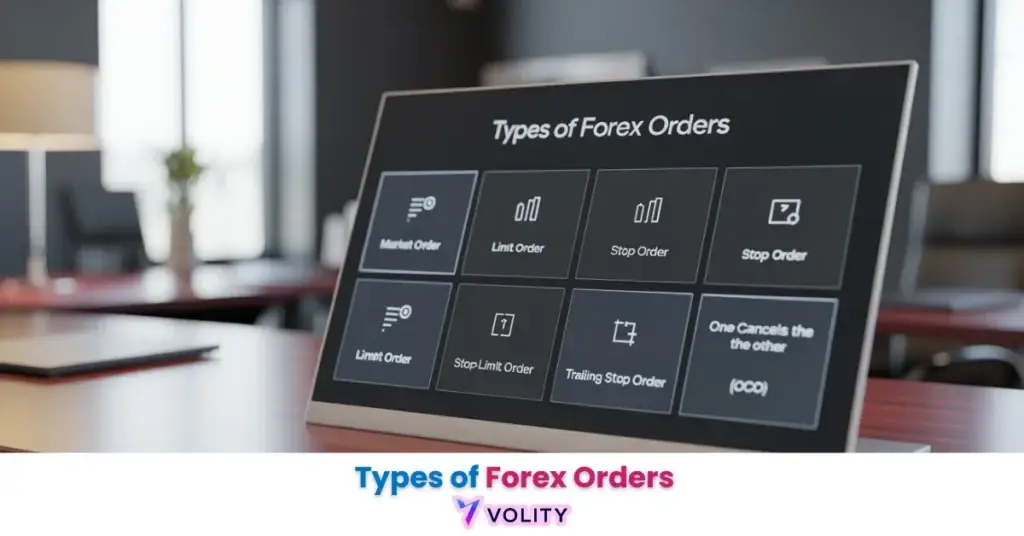

Forex orders are structural primitives that translate a trade plan into platform behavior, categorized into market, pending, and risk-management types. These instructions define how and when capital is committed to the $9.6 trillion daily market. In 2026, retail execution speeds have reached a 60ms average, with top-tier ECN brokers delivering sub-1ms latency to match institutional algorithmic performance.

Types of forex orders function as the critical link between a trader’s analytical hypothesis and the actual commitment of capital. These instructions determine the exact conditions under which a trade is triggered, filled, or closed to protect profit. They serve as the foundational language of the $9.6 trillion daily currency market in 2026.

The 2026 trading landscape is defined by the migration to cloud-native platforms and the “T+1” settlement transition. Investors utilize advanced conditional orders to navigate a market increasingly dominated by high-frequency AI algorithms and institutional liquidity sweeps.

While understanding Types of Forex Orders is important, applying that knowledge is where the real growth happens. Create Your Free Forex Trading Account to practice with a free demo account and put your strategy to the test.

What are the primary types of forex orders?

Forex order types are specific software instructions that determine the price, timing, and quantity parameters of a market transaction. Every order placed on a forex platform falls into one of three structural categories: immediate execution (market orders), delayed execution (pending orders), or protective exit (stop-loss and take-profit). Understanding these categories allows traders to match their analytical edge to the precise execution method that maximizes probability of success.

Orders differ fundamentally based on whether they prioritize speed or price. A market order executes immediately at the current ask price (for buys) or bid price (for sells), sacrificing price precision for guaranteed entry. A limit order waits indefinitely at a target price, sacrificing entry certainty for guaranteed fill price. Each order type serves a specific market condition, scalpers require market orders for sub-second entries, while swing traders rely on limit orders to avoid overbuying at resistance zones.

Risk management layers demand that every open position includes protective orders. A stop-loss order automatically closes a losing trade if price moves against the position by a predetermined amount, preventing catastrophic drawdowns. A take-profit order automatically closes a winning trade at a target level, crystallizing profits before reversal. Together, these bracketing orders create a complete risk envelope around each position.

In 2026, sub-100ms execution is the retail standard; any latency above 100ms is considered “slow” and increases slippage risk during news events (TrustFinance, 2026). This performance improvement means retail traders on quality brokers can now compete with institutional desks on execution speed alone, the true competitive advantage has shifted to strategy and psychology.

The Operational Families of FX Orders

Order classification identifies the difference between immediate liquidity taking and passive liquidity providing. Market orders are classified as “Aggressive” because they absorb whatever liquidity exists at the current market price, immediately moving the bid-ask spread in the trader’s disfavor. A trader executing a market buy on EUR/USD when the spread is 1.0 pip wide instantly loses that 1 pip to the spread, even before considering slippage.

Limit orders are classified as “Passive” because they provide liquidity to other traders. A trader placing a limit buy order below the current ask price is offering to buy at a specific price if the market reaches that level. If the market drops to touch the limit price, the order executes at exactly that level without spread cost. Passive orders serve long-term accumulation strategies where entry speed is less important than entry price.

Ready to Elevate Your Trading?

You have the information. Now, get the platform. Join thousands of successful traders who use Volity for its powerful tools, fast execution, and dedicated support.

Create Your Account in Under 3 MinutesImmediate vs. Pending Execution: Choosing the Right Entry

Execution methodology determines whether a trader prioritizes the speed of entry through market orders or price precision through limit orders. Market orders guarantee immediate fill at the current market price, which is essential for traders who need exposure instantly, news traders often use market orders to enter the market within 500ms of an economic data release. Limit orders guarantee a specific fill price or better, which is essential for swing traders accumulating positions at historical support zones.

High-tier ECN brokers now deliver execution speeds as low as 0.35ms in 2026, allowing retail traders to compete with institutional HFT desks (InvestinGoal, 2026). This speed improvement has narrowed the execution advantage that institutional traders once held over retail participants. Modern retail platforms using cloud-native infrastructure deliver fills so fast that a trader’s psychology and strategy have become more important than raw latency.

Stop orders function as hybrid instruments that combine the patience of limit orders with the urgency of market orders. A buy stop order sits dormant above the current price, automatically converting to a market buy if price touches the stop level. This mechanism allows traders to capture breakouts above resistance by having a buy order pre-positioned to trigger automatically. Similarly, a sell stop below the current price triggers automatically if price drops to that level, executing a market sell that allows traders to short breakdowns below support.

Limit orders allow traders to set target prices that attract institutional liquidity and improve fill quality. Understanding session-specific timing helps traders select order types appropriate for each trading window’s volatility profile.

Advanced Conditional Orders: OCO and OTO Explained

Conditional order logic identifies the relationship between multiple trade legs, where the execution of one instruction triggers or cancels another. OCO (One-Cancels-the-Other) orders automate straddle strategies by placing two pending orders, one buy and one sell, on opposite sides of the current price. When price moves decisively in one direction and triggers one of the orders, the other order automatically cancels, preventing accidental double-entry. This mechanism allows traders to capture breakouts without monitoring the chart during uncertain periods.

OTO (One-Triggers-the-Other) orders automate the entire trade lifecycle by linking an entry order to exit orders. When an OTO buy stop at 1.2850 executes, the system automatically attaches a take-profit order at 1.2950 and a stop-loss order at 1.2800, creating a complete risk envelope without manual intervention. This automation prevents the emotional hesitation that often causes traders to enter without pre-planned exits, a leading cause of blown accounts.

Stop-limit orders combine a breakout trigger with a maximum slippage cap, ensuring that breakout trades execute within a predefined price range. A sell stop-limit at 1.2800 (trigger) / 1.2750 (limit) means the trade only executes if price drops to 1.2800, but will not execute below 1.2750. This mechanism protects against catastrophic gaps on low-liquidity breakdowns, though it carries the risk of non-execution if price gaps past the limit level without touching it.

Real trading example: In June 2026, a trader placed an OCO order before the BoE rate decision, with a Buy Stop at 1.2850 and a Sell Stop at 1.2750, separated by 100 pips to capture the expected volatility. When the Bank of England announced an unexpected rate hike, the market surged on sterling strength, triggering the Buy Stop at 1.2850 and automatically canceling the Sell Stop, protecting the trader from a potential whip-saw double-entry that would have destroyed capital. Past performance is not indicative of future results.

Order Execution Speed Benchmarks in 2026

Technical performance benchmarking identifies the execution latency across different broker models and technology tiers in 2026. Execution speed directly impacts slippage, the difference between the price at which a trader expects to execute and the actual fill price. During volatile news releases, spread widening alone can consume 10-15 pips of intended profit if orders execute slowly.

| Broker Category | Avg. Execution Speed (2026) | Optimal Strategy | Risk Profile |

| Ultra-Low Latency ECN | 0.35ms – 0.60ms | Scalping / HFT | Low Slippage |

| Top-Tier Standard | 3ms – 15ms | Day Trading | Medium |

| Mainstream Retail | 20ms – 50ms | Swing Trading | High Gap Risk |

| Social / Copy | 150ms – 300ms | Position Trading | High Slippage |

| Market Maker | 100ms+ | Basic Investing | Variable Spreads |

Source note: Data compiled from InvestinGoal and FXEmpire 2026 Performance Audits.

Ultra-low latency brokers using direct market access (DMA) to liquidity pools execute scalping strategies where 2-3 pip profits depend on fills within 100ms. Top-tier standard brokers serve day traders who need 10-20 pip moves to offset transaction costs, tolerating slightly slower execution. Mainstream retail brokers serving swing traders accept 20-50ms latency because swing moves typically exceed 50 pips, making execution speed less critical. Social and copy trading platforms sacrifice speed for simplicity, automating follower positions with 150-300ms delays acceptable only for position traders working 1-week timeframes.

Best Execution and the 2026 MiFID III Framework

Regulatory best-execution standards identifies that “Total Consideration” must include price, speed, and settlement reliability for all retail orders. MiFID III (Markets in Financial Instruments Directive III) established in 2026 eliminated the quantitative requirement to publish real-time trading data (RTS 27/28), replacing it with a qualitative Order Execution Policy that brokers must document and publish. Brokers must now demonstrate that their order routing decisions achieve the best possible result across price, cost, speed, and reliability, not just price alone.

The 2026 PFOF Ban represents a structural shift in how retail brokers monetize order flow. Previously, retail brokers earned rebates from market makers for routing retail orders to their venues, creating a conflict of interest where execution quality was sacrificed for rebate size. The EU-wide ban on Payment for Order Flow forces brokers to justify routing decisions based purely on execution quality metrics, eliminating the perverse incentive to route orders to slower, lower-quality venues that paid higher rebates. This regulatory change will progressively improve retail execution as brokers compete on speed and fill accuracy rather than rebate size.

The transition to T+1 settlement in 2027 will compress the time window for dispute resolution and fund transfer from two days to one day. Brokers must settle all trades with counterparties within 24 hours, increasing counterparty risk management costs and potentially reducing margin capacity during volatile markets. Traders should expect modest spread widening during the T+1 transition as brokers adjust risk models to the tighter settlement window.

Proper risk management frameworks explain how order types combine to create complete trade plans that protect capital systematically. Regulatory details are available through ESMA: MiFID II Review and Order Execution Policies 2026 and the KPMG: The EU Ban on Payment for Order Flow (PFOF) 2026.

Step-by-Step: Mastering Your Execution Workflow

Systematic order entry represents the final step in translating technical analysis into a live-market commitment. The workflow begins by analyzing the current spread before placing any order. A 1.5-pip spread on EUR/USD means a trader loses 1.5 pips immediately upon entry with a market order, requiring the market to move at least 1.5 pips in their direction just to break even. During Asian session low-liquidity periods, spreads widen to 3-4 pips, doubling the break-even requirement.

Step 2 involves selecting the order type that matches the intended holding period and market condition. A scalp trade targeting 5 pips of profit in 30 seconds requires a market order because the market won’t wait for a limit order to execute during a 30-second window. A swing trade targeting 50 pips over three days can use a limit order to enter at a better price even if it delays entry by hours. Matching order type to strategy reduces transaction costs and improves edge.

Step 3 requires setting the Time-in-Force parameter that governs how long the order remains active. GTC (Good ‘Til Canceled) orders remain active indefinitely until filled or manually removed, suitable for limit orders targeting key support levels. GTD (Good ‘Til Date) orders expire at a specified date/time, preventing ancient limit orders from executing unexpectedly months later. FOK (Fill-or-Kill) orders cancel immediately if they cannot execute at the requested price, essential for high-frequency trading where partial fills create unwanted exposure.

Step 4 requires attaching protective brackets, a stop-loss order below the entry and a take-profit order above the entry, before the trade is executed. This pre-planning prevents the emotional override that occurs when trades move against a trader: instead of panic selling at a loss, the automatic stop-loss triggers. Modern platforms support bracket orders that link stop-loss and take-profit orders to the primary entry, ensuring they activate only if the entry executes.

Identifying the price levels where stop-loss and take-profit orders should be placed requires analyzing recent swing points and support/resistance zones to determine optimal exit levels. Calculating stop-loss distances that account for volatility and average daily range ensures that protective orders absorb normal price fluctuations without being triggered by random noise.

Turn Knowledge into Profit

You have done the reading, now it is time to act. The best way to learn is by doing. Open a free, no-risk demo account and practice your strategy with virtual funds today.

Open a Free Demo AccountKey Takeaways

- Types of Forex Orders are the structural primitives used to manage entry, exit, and risk in the $9.6 trillion daily market.

- Market orders prioritize immediate execution at the current ask or bid, while limit orders prioritize price precision over speed.

- Execution speeds in 2026 have reached an industry average of 60ms, with ultra-low latency ECNs delivering sub-1ms results.

- The 2026 PFOF ban ensures that European brokers prioritize execution quality and transparency over rebate-driven order routing.

- Conditional orders, including OCO and OTO, allow traders to automate complex multi-leg strategies and minimize emotional interference.

- Total Consideration remains the MiFID III standard, requiring brokers to balance price, cost, and speed for every retail transaction.

Frequently Asked Questions

This article contains references to forex order types, execution standards, and Volity, a regulated CFD trading platform. This content is produced for educational purposes only and does not constitute financial advice or a recommendation to execute trades using any specific order type. Always verify your broker’s order execution standards and ensure they comply with 2026 MiFID III regulations. Some links in this article may be affiliate links.