Investing in financial products involves risk. Losses may exceed the value of your original investment.

Nvidia gtc ai is a core topic for traders in 2026. The complete guide follows.

Nvidia’s GTC showmanship revives the AI trade, and traders smell a clean setup

San Jose felt like theatre on Monday. Jensen Huang, Nvidia’s chief executive, spent two hours at GTC 2026 describing “AI factories”, agentic systems and physical AI. Meanwhile, the market treated the keynote as a permission slip to lean back into the AI momentum book.

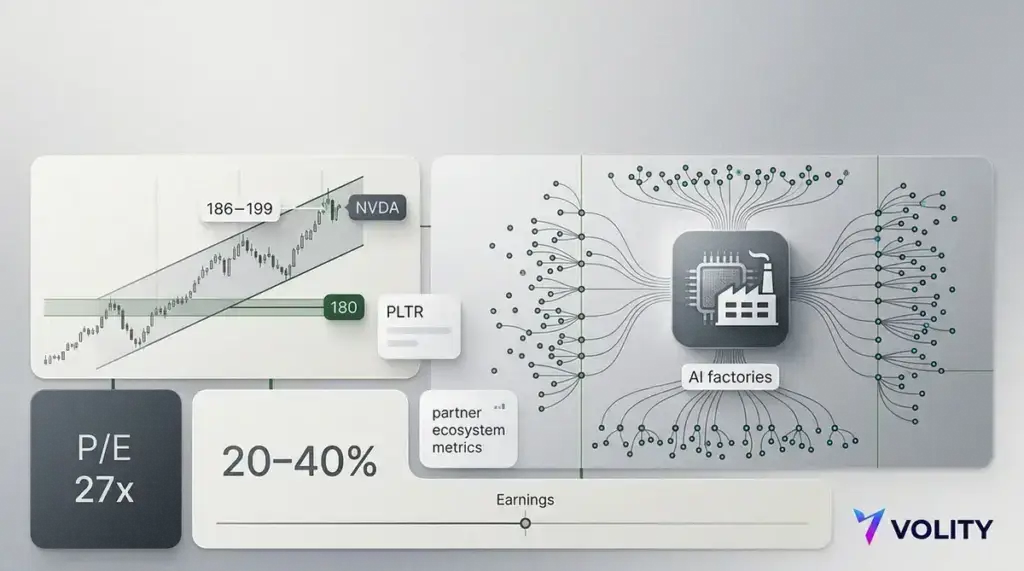

Nvidia shares traded in the $186 to $199 zone around the event, after a choppy patch that left plenty of traders hunting for a tidy dip. However, the mood shifted as Huang tied new products to a familiar promise. Accelerated computing cuts costs, expands capability and pulls more workloads onto Nvidia’s stack.

He avoided any single headline-grabbing bookings figure. Instead, he stacked breadth on breadth. Huang talked up an ecosystem of roughly 450 partner companies and framed the prize as “a hundred trillion dollars of industry”. Therefore, the pitch was less about one quarter’s demand and more about Nvidia as default infrastructure.

That matters because the market still trades Nvidia like a capex proxy. If hyperscalers keep spending, Nvidia prints. If they pause, the multiple compresses first and questions arrive later. So traders listened for a tell on durability, and the tone stayed bullish.

Targets drift higher, but valuation keeps its teeth

Consensus remains a tailwind. Across widely followed analyst averages, the central case still points to roughly 20% to 40% upside from the high-$180s. Meanwhile, the spread between highs and lows stays wide enough to keep options desks busy.

At the same time, Nvidia is no longer “cheap” in the lazy sense. A forward multiple around the high-20s can look sensible next to growth forecasts. However, it also leaves little forgiveness for any capex wobble or supply hiccup. Therefore, execution still matters more than storytelling, even when the storytelling is good.

Technicals look like a reset, not a breakout yet

Price action around the $180s has started to look like a pivot zone, with traders watching the 20-day, 50-day and 200-day averages converge nearby. RSI readings have sat near neutral rather than stretched. Consequently, the chart reads like a coiled spring, but not one that has definitively launched.

In plain terms, the bulls have a level to defend. Meanwhile, the bears need a clean breakdown to argue the keynote bump was just fumes.

Palantir has tried to surf the same enterprise AI wave, announcing partnerships across data and services, including names like Databricks, Accenture, Snowflake and Lumen. That kind of list supports the adoption narrative. However, traders should treat any stale price level as worthless until the live tape confirms it.

Therefore, PLTR remains more of a momentum watch than a thesis anchor. If Nvidia is infrastructure, Palantir is a workflow bet, and the market will price them differently when volatility rises.

What to watch next

GTC did what it usually does. It refreshed the story, widened the runway and reminded everyone that Nvidia sells the picks, shovels and operating manual. However, the next clean catalyst is still earnings, where “beat and raise” is the only language that keeps the multiple comfortable.

- For dip buyers, the $180 area matters as near-term support, because it anchors the current reset.

- For momentum traders, strength above the recent $190s band would matter more than any slide deck.

- For options desks, the wide target range keeps skew and defined-risk structures relevant.

- For everyone, capex tone from hyperscalers remains the macro switch for the whole AI complex.

By the numbers

- NVDA price zone discussed: $186 to $199

- Partner count cited on stage: about 450

- Upside implied by many 12-month targets: roughly 20% to 40% from the high-$180s

- Forward P/E referenced by bulls and bears: about 27x

- Keynote: March 16, GTC 2026 week

Key takeaways

- Nvidia’s keynote reinforced ecosystem lock-in, which supports the “buy the dip” reflex.

- Valuation still demands clean execution, so position size should match your tolerance for capex shocks.

- Support near $180 is the line traders will fight over; a hold invites upside tests.

- Palantir fits the enterprise AI narrative, but it needs real-time confirmation before chasing.

For more on this topic see our deep-dives on TSMC Stock Surges on AI Chip Demand as Retail Earnings Loom, Argan (AGX) Stock: Earnings, Power Demand and Buy Case, and FedEx Earnings: Guidance, Cost Pressure and Freight Spin-Off Risk.

What our analysts watch: Three reads turn the GTC event into a sized position rather than a headline reaction. Hyperscaler capex commitment quality (Microsoft, Google, Amazon, and Meta capex run-rate translates into NVDA revenue with a one-to-two-quarter lag; the GTC week typically produces fresh capex commentary from executive interviews that confirms or revises the trajectory). Inference-versus-training revenue mix (the structural bull case requires inference-driven revenue to ramp into the multi-billion-dollar quarterly run-rate; GTC product disclosures around inference-optimised silicon are the leading indicator of the mix-shift trajectory). Sovereign-AI deal-flow pace (the multi-billion-dollar deals with Saudi Arabia, the UAE, and emerging-market governments are the structural growth lever beyond the hyperscaler base; deal-flow announcements during GTC week confirm the trajectory). The ESMA investor protection publishes the 10-Q and 10-K filings that anchor the disclosure read, the StockCharts ChartSchool reference on support levels covers the technical framework, and the Nasdaq market data tracks the live volume context. Volity offers U.S. AI-equity CFD execution under CySEC oversight via UBK Markets (licence 186/12), with entities in Saint Lucia, Cyprus, and Hong Kong.

Frequently asked questions

How does NVDA support test quality differ from broader AI-stock support tests?

It differs because NVDA carries the structural-bellwether role for the AI-rally complex, which means the support test is read as a sector-wide signal rather than a single-name technical event. A clean NVDA support defence on the GTC week typically lifts the broader AI-stock complex by 2 to 5 percent within two sessions; a clean breakdown produces correlated weakness across the AI peer group regardless of individual company fundamentals. The disciplined response is to size the position around the sector-wide implication rather than the single-name move, because the marginal trade is the AI-rally thesis rather than the NVDA-specific event.

What does hyperscaler capex commentary reveal during GTC week that quarterly earnings do not?

It reveals the forward run-rate adjustment that quarterly earnings only confirm with a quarter lag. Hyperscaler capex commentary during GTC typically arrives through executive interviews, partnership announcements, and conference panel disclosures that surface forward-looking spend commitments which the quarterly filings only ratify in the next reporting cycle. The structural read is that the GTC commentary is a leading indicator with a one-to-two-quarter horizon; the quarterly earnings is a trailing indicator. The clean trade thesis weights the GTC commentary heavily for the next-two-quarter positioning and the quarterly earnings for the trailing confirmation.

How seriously should traders treat the AMD MI-series competitive response?

The competitive response carries multi-quarter relevance but limited near-term price impact for NVDA. The structural mechanic is that hyperscaler capex commits are typically multi-vendor at the headline level (the major buyers want supply diversification) but concentrate revenue at the leading vendor through the actual deployment cycle because the software stack maturity differential favours the incumbent. AMD MI-series share gains in the 5 to 15 percent range over multiple quarters do not invalidate the NVDA structural thesis; share gains above 25 percent over multiple quarters would. The current trajectory sits in the lower-band, which keeps the NVDA thesis intact through the GTC cycle.

Does the sovereign-AI deal-flow trajectory carry geopolitical risk that traders should price?

It carries meaningful geopolitical risk that traders should price as a tail-risk discount rather than a base-case cap. The Saudi Arabia, UAE, and emerging-market sovereign-AI deals are subject to U.S. export-control regimes that can change with policy cycles, which introduces a multi-billion-dollar revenue-stream contingency that does not exist in the hyperscaler base. The disciplined treatment is to apply a 10 to 20 percent risk discount to the sovereign-AI revenue stream in the multi-quarter forecast, which keeps the structural thesis intact while pricing the contingency. The export-control regime has so far accommodated the deal-flow with case-by-case licensing; the structural risk is a regime change that compresses the licensing pace, which would re-rate the multiple rather than break the rally.

Related guides

- Best AI stocks to invest in

- Stocks investing for beginners

- Best stock trading platforms in Europe

- Best trading platforms

- Risk management

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.