Investing in financial products involves risk. Losses may exceed the value of your original investment.

Batl dxyz spacex is a core topic for traders in 2026. The complete guide follows.

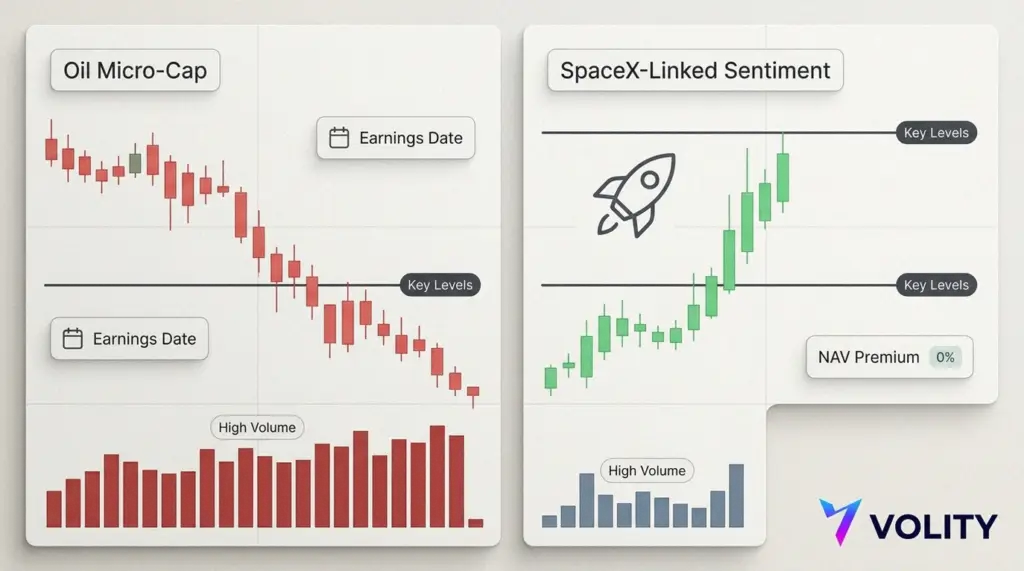

Daily trader watch: Volatility bites back in oil and space bets

Two very different corners of the market put on the same show recently: leverage, thin floats, and traders testing how far a story can run before it snaps. Battalion Oil (BATL) sank 17.51% to $9.14 by the close after printing $11.08 the prior session. Meanwhile, Destiny Tech100 (DXYZ) jumped 9.27% to $26.52, as SpaceX chatter kept a speculative bid under a closed end fund that thrives on buzz.

However, the action was not symmetrical. BATL’s tape looked like forced selling into fragile support. DXYZ’s looked like a relief rally that still needs follow through. Therefore, both names now sit at levels where the next hour can matter more than the next quarter.

BATL: the oil driller’s rollercoaster finds gravity

BATL has spent weeks reminding traders that size does not equal stability. Earlier this month, its market value briefly looked inflated by momentum, with figures cited as having swelled to about $307.91m around March 13 after a violent run. The company also talked up growth moves, including the all stock Sundown deal. Meanwhile, the share price itself has ricocheted from February lows near $5 to March highs around $27, then straight back into the single digits.

On March 24, the selling did not arrive politely. BATL fell as much as 34.57% intraday and traded roughly 4.4m shares on the session, which is heavy for a micro cap.

Volume like that tends to expose the real balance of power. In this case, sellers appeared to control the day, not just the close.

Early March 25 prints around $7.70 only sharpened the question: was March 24 capitulation, or simply the first air pocket?

Fundamentals offer little comfort in the short run. Trailing twelve month revenue sits around $166m, yet losses have dragged earnings per share to about -2.24.

That mix can work in a rising oil tape, although it rarely survives a momentum unwind. Traders now focus on the calendar, since BATL’s next earnings are slated for March 30.

Therefore, positioning into that date may matter more than any technical pattern drawn on a quiet chart.

Set ups are stark. If $9 holds on a closing basis, a reflex bounce towards $11 can appear, especially if crude stabilises. However, a failed reclaim of $9 often brings fast tests of prior lows. If the stock cannot defend the $7 to $9 zone, the tape can start searching for liquidity below it.

DXYZ is a different beast. It is a closed end fund built to give public market access to private tech stakes, which means its price can detach from its underlying value for long stretches. On March 24, the stock rose from about $24.27 to $26.52 on roughly 3m shares, as traders chased another round of SpaceX related excitement.

Yet the broader month has been messy. DXYZ has swung hard from highs near $28.42 in late February to a recent low around $23.48.

YTD performance has been cited near -59%, even as the one year number still looks bizarrely strong. That is the point with this product.

You are not buying steady compounding. You are renting sentiment.

The key tell remains the premium to its net asset value. As of March 23 figures, the shares traded at roughly $24.27 against a NAV near $19.97, or about a 21.53% premium. That is lower than the wild extremes seen over the past year, although it still leaves plenty of room for air to come out if the story cools. Meanwhile, when the fund is hot, it can stay irrational for longer than a tidy valuation model expects.

For traders, the levels are clean. A push through $27 to $28 can trigger momentum buying, since that zone has acted like overhead supply. However, if the stock rolls back under $25 after the open, the move can look like a one day squeeze rather than a new leg.

By the numbers

- BATL March 24 close: $9.14, down 17.51%, about 4.4m shares traded

- BATL intraday move March 24: down as much as 34.57%

- DXYZ March 24 close: $26.52, up 9.27%, about 3m shares traded

- DXYZ NAV gap: $24.27 price versus $19.97 NAV, about 21.53% premium

- Next key date: BATL earnings March 30

Key takeaways

- BATL is trading like a de lever event, so treat bounces as tactical unless $9 holds convincingly.

- Because earnings hit March 30, implied volatility and positioning can dominate the tape before fundamentals do.

- DXYZ remains a premium trade, therefore price action can diverge sharply from NAV for days or weeks.

- Watch $27 to $28 on DXYZ for momentum continuation, while $25 is the line between squeeze and fade.

- In both names, volume is the signal, since these moves can reverse without warning on thin liquidity.

For more on this topic see our deep-dives on Stock Market Guide: Earnings, Analyst Moves and Breakouts, Gold Price Outlook and Dow Rally: Reading Overbought Signals, and Nvidia GTC and the AI Stock Rally: How NVDA Tests Key Support.

Alexander Bennett notes: Three filters separate tradable thin-float setups from chart shapes that punish symmetric positioning. Float-to-volume ratio (when daily volume runs above 5 percent of public float, the price action carries fundamental information about positioning rather than noise; below that threshold, intraday moves are flow-driven and frequently mean-revert).

Closed-end fund premium versus NAV trajectory (a structural premium of more than 20 percent above NAV is unstable; the historical pattern is that the premium compresses toward NAV during sector-stress windows and expands again during sentiment-recovery windows, which makes the premium itself a tradable feature rather than a static valuation input). Catalyst calendar overlay (BATL with earnings on March 30 carries asymmetric path risk into the announcement; the disciplined practice is to size for the catalyst-overlay distribution rather than to bet on the directional resolution).

When the three filters align, thin-float trading becomes a structured discipline. When they are absent, the same chart shape produces the casino distribution that defines retail underperformance in the segment.

Frequently asked questions

Because the premium itself reflects the marginal trader willingness to pay above the underlying-asset value for the structural feature of the wrapper (public-market access to a private-asset basket plus liquidity), and the premium expands and compresses on a different schedule than the underlying NAV. A 21.53 percent premium is below the historical extremes for DXYZ but well above zero, which means the wrapper carries embedded mean-reversion risk that pure NAV analysis misses. Traders who model the premium trajectory separately from the NAV trajectory capture the wrapper-specific dynamic that drives the bulk of the daily price action; traders who treat the premium as a static feature systematically misprice the position. The Investopedia reference on closed-end fund premium and discount mechanics covers the analytical framework.

What does the BATL one-month range from 5 to 27 dollars and back reveal?

It reveals that the float profile and the leverage stack on BATL produce a return distribution that is fat-tailed in both directions, with no meaningful mean-reversion anchor at any level inside the trailing month. The structural consequence is that classical position-sizing rules calibrated to large-cap volatility distributions systematically under-account for the path-dependent stop-out risk inherent in the name; positions sized for a 5 percent stop will be stopped out by ordinary intraday flow rather than by genuine thesis invalidation. The disciplined sizing approach scales position size to fit a stop band of 15 to 25 percent rather than 5 to 10 percent, and accepts the reduced position-level dollar exposure as the cost of trading the volatility distribution honestly. The SEC investor alert on low-float securities documents the regulatory backdrop.

How should traders position into the March 30 BATL earnings catalyst?

The disciplined frame sizes the position for the path-dependent distribution rather than the directional resolution. The historical pattern in micro-cap energy names with comparable balance sheets is that the post-earnings range expands two to four times the trailing daily range, with a path that punishes symmetric directional positioning because the pre-announcement positioning unwinds in both directions during the first session after the print. Defined-risk options structures (verticals or risk reversals at meaningfully wide strikes) handle the path-dependence better than spot positioning for accounts without specific edge in either earnings-revision modelling or insider-flow tracking. The structurally cleaner expression is the post-earnings entry once the initial range has resolved, which captures the new positioning regime without the catalyst-overlay risk.

The closed-end fund wrapper provides public-market access to the SpaceX-related private-asset basket, which is the structural feature that supports a long-term thesis. The wrapper-specific risks (premium compression, fund-management fee drag, governance friction during private-asset valuation marks) impose a multi-year cost that the long-term holder must price against the underlying private-asset return distribution. The honest framing is that DXYZ is a hybrid instrument: the underlying NAV reflects the private-asset basket, and the wrapper premium reflects the public-market sentiment toward the wrapper itself; long-term holders need to evaluate both legs rather than treating the position as pure SpaceX exposure. The Nasdaq DXYZ market activity page tracks the listed-equity reference price.

Related guides

- Stocks investing for beginners

- Day trading platforms

- Best trading platforms

- Risk management

- Risk-reward ratio

Volity operates a trading platform and also publishes educational and analytical content about trading. The content on this page is for educational purposes only and should not be considered financial advice. Volity may benefit commercially when readers open trading accounts through links on this site.

Our content is produced and reviewed under documented editorial standards; comparison and review methodology is published here.